Capturing Mideast Crash-Out Optionality: Case Study for Hedge Funds, Endowments, and Pension Funds

EIS/KSA ETF Barbell with beta hedge via East Asian EM Short— 13% Excess Returns in March 2026

Executive Summary

Opening Salvo:

Pre-market on 2 March 2026— the first US Trading Day of the USA-Iran War— DuLac Capital Advisory L.L.C. published an institutional Thought Piece underscoring a risk-management way for institutional capital allocators to deliver alpha during a time of war induced dispersion.

Geopolitical X Economic Macro Risk Factor Dispersion:

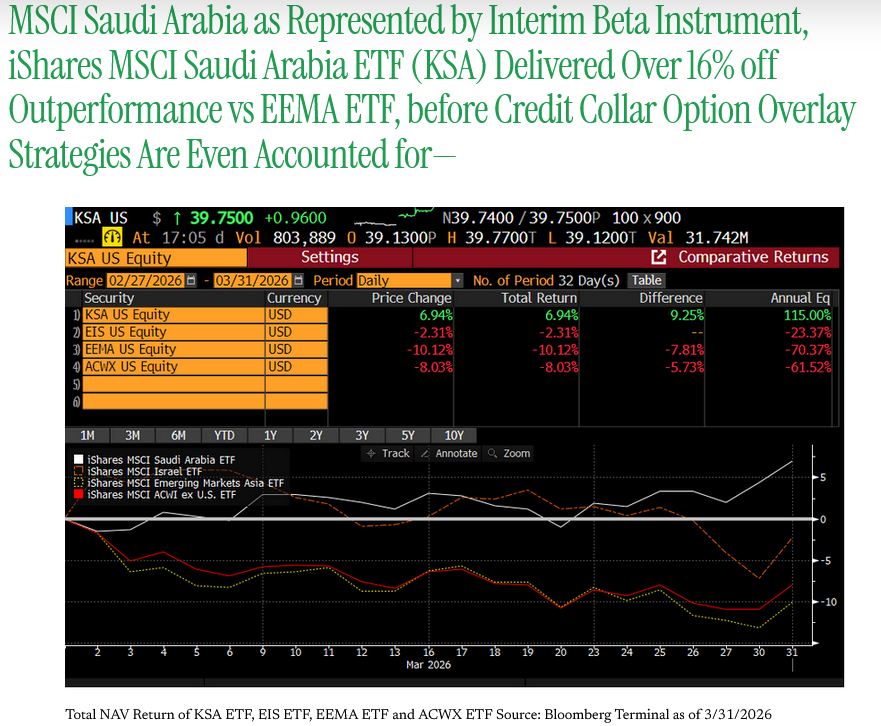

Amid escalating IRGC-linked disruptions, potential Strait of Hormuz tensions, and commodity supply shocks, a 70/30 KSA (Saudi Arabia)ETF/EIS (Israel) ETF barbell paired with a delta-neutral short for funding— and to hedge beta risk— via the iShares MSCI Emerging Markets Asia ETF (EEMA) delivered 13.47% excess return as of 3/31/2026.

KSA alone outperformed EEMA by more than 16% on a total NAV return basis before options overlays, while maintaining tight tracking error (<10bp versus its benchmark).

Why it worked:

The structure provided structurally long investors with convex exposure to Mideast dispersion—harvesting volatility premium through options while neutralizing directional beta. This case study demonstrates how hedge funds, endowments, and pension plans constrained by benchmark mandates can embed high-conviction optionality on geopolitical tail risks without forced liquidation of core equity exposure. The strategy turned March’s realized volatility spikes into a premium-harvesting opportunity, with muted ETF redemptions signaling strategic and tactical allocator institutional conviction.

Client Challenge

March 2026 tested Mideast resilience in real time. IRGC attacks on Gulf infrastructure, market closures (e.g., UAE), and supply-chain pressures on energy routes created asymmetric risks for commodity-sensitive regions, particularly EM Asia.

Traditional long-only allocations faced drawdowns in benchmarks like MSCI ACWI ex-USA (ACWX) and EEMA, while energy “toll-booth” exposures and select DM-adjacent tech/financials showed relative strength.

Structure of the Barbell Pair Allocation:

Many institutions remain structurally long MSCI DM-ex-USA or MSCI EM IMI constituents, including meaningful weights to Israel (via EIS) and Saudi Arabia (via KSA). Rather than exiting these positions amid uncertainty, the EIS/KSA barbell offered a disciplined way to overweight resilience factors (energy infrastructure + tech depth) while shorting the most vulnerable commodity-beta proxy (EEMA) for beta risk hedging.

The original strategy published on March 2, 2026, positioned the barbell as a “dispersion resilience vehicle” for long-biased mandates.

By month-end, the live results validated the thesis with strong risk-adjusted outperformance.

Strategy Overview— Core Construction

Long Barbell: 70% iShares MSCI Saudi Arabia ETF (KSA) + 30% iShares MSCI Israel ETF (EIS)

Weights approximate February 2026 market-cap contributions to MSCI ACWI ex-USA.

KSA provides energy/infrastructure resilience and “toll-booth” economics.

EIS adds technology and financials depth with growing options liquidity (≈50% of top holdings have US-listed options).

Delta-Neutral Hedge: Short position in EEMA (or ACWX for broader coverage) to isolate dispersion and neutralize broad EM/IRGC beta.

Options Overlay: Covered collars, vertical spreads, calendars, or diagonals to fade tail risk and harvest implied-versus-realized volatility divergence. Premiums are budgeted in basis points of portfolio risk budget.

Objective

Generate convex payoffs on Mideast “crash-out” scenarios—supply disruptions, infrastructure stress, and recovery dynamics—while preserving participation in any de-escalation or reconstruction upside. The structure functions as a volatility sponge, particularly effective when realized vol lags implied vol in the first 10–14 days of tension.Suitability

Ideal for:

Hedge funds seeking tactical dispersion trades with defined risk.

Endowments and pensions managing benchmark-relative volatility in global equity sleeves.

Risk-budgeted satellite allocations (typically 2–5% of equity book).

Results

Live Execution (Strategy Idea Publishing: 3/2/2026 to 3/31/2026)

The barbell was funded delta-neutral against high beta EEMA.

Key implementation notes:

Liquidity remained functional despite volatility spikes.

Creation/redemption flows in KSA and EIS were muted relative to the ~40–50% rise in 20-day realized volatility, contrasting with sharper drawdowns elsewhere.

Options overlays captured premium as implied volatility diverged from realized paths in the opening phase of the flare-up.

Key Performance Metrics (as of 3/31/2026)

KSA vs. EEMA: >+16% outperformance on total NAV return (pre-overlay)

KSA vs. ACWX: >+12% absolute outperformance since early March war-start window

Tracking Error: KSA maintained <10bp (9bp) versus MSCI Saudi Arabia 25/50 IMI Index

Volatility Dynamics: KSA ~40% 20-day realized vol increase; EIS ~50% spike—both with limited redemption pressure

Risk-Adjusted Outcome: Strong relative performance versus MSCI DM-ex-USA and MSCI EM/DM Asia benchmarks

EEMA, as a commodity-sensitive proxy, absorbed the bulk of the supply-shock beta, enabling the short leg to contribute meaningfully to the excess return. The barbell’s tech-energy dispersion profile delivered resilience where broader EM Asia faced headwinds.

13% Excess Returns (Long KSA/EIS, Short East Asian EM (EEMA) in March 2026

Whatever it is, the way you tell your story online can make all the difference.

It all begins with an idea. Maybe you want to launch a business. Maybe you want to turn a hobby into something more. Or maybe you have a creative project to share with the world. Whatever it is, the way you tell your story online can make all the difference.