Update– EIS/KSA Barbell Strategy: ETF/Index Maxxing for Beta Management and Optionality during Rising Mideast Energy Supply Chain Disruptions

Bottom Line Up Front (Executive Summary)

Systematic Commodity Supply Chain Shock Catalyst: The Surprising Strait of Hormuz closure is no longer a regional issue; it is a systemic "input cost" tax on the world’s two most energy-dependent manufacturing hubs: EM Asia (iShares MSCI EM Asia ETF: EEMA) and Developed Europe (e.g. iShares MSCI Europe IEUR).

The Exposure:EEMA is facing a double-bind— 40% of China’s oil and 25% of its LNG are currently idled per CSIS due to the Strait of Hormuz closure, while IEUR faces a second "energy winter" as Qatari LNG force majeure events halt shipments to EU terminals.

The Strategy: Last week (3/2/2026-3/6/2026), the EIS/KSA Barbell acted as a volatility sponge vs EM and DM-exUSA. While EEMA and IEUR see margin compression due to energy spikes, the KSA component captures the "scarcity premium" and EIS provides tech-resilience that is uncoupled from the manufacturing supply chain.

The Allocation: Institutional allocators should look to fund this barbell by trimming overweight positions in energy-importing regions (EEMA/IEUR) that have reached a "volatility floor."

Case Study— UAE ETF Liquidity as a Buffer: ETFs like the iShares MSCI UAE ETF (UAE) provided vital liquidity and beta management for institutional investors, even when the underlying local equity markets were closed due to regional kinetic Shaheed drone and missile attacks by the IRGC.

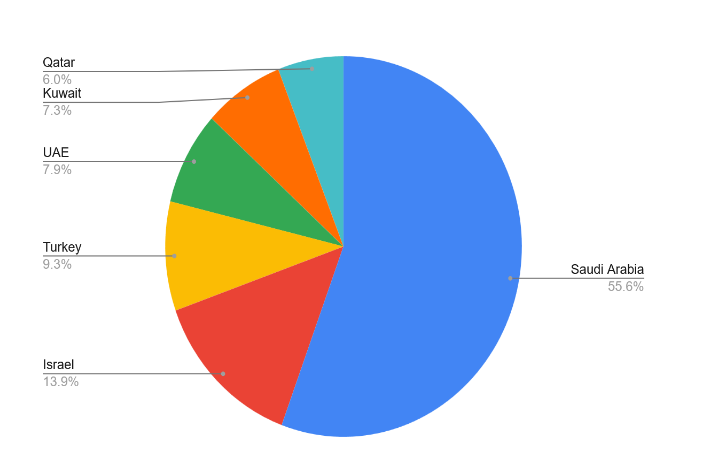

MSCI ACWI-exUSA IMI Index– GCC plus Israel Exposure by Market Cap Component (as of 02/28/2026)

Source: MSCI, Google Gemini as of 2/28/2026

1. Introduction: The General’s Temple Calculations:

General Sun Tsu famously wrote in the Art of War, “The general who wins a battle makes many calculations in his temple before the battle is fought.” With the surprising closure of the Hormuz Strait which has chocked off oil and LNG from commodity sensitive East Asia and Europe, concerns are emerging about the risks of a business cost input and consumer commodity shock that could throw the global economy off its course.

This was a key driver why MSCI EM jump from 16% on a rolling 20 Day annualized basis to 27%: with implied volatility jumping standard deviations higher. It seems the market did not listen to Peter Orszag of Lazard at Davos this past January when he said on Bloomberg TV that he thinks there is an underpriced risk of war against the IRGC– due to conversations the former White House official had prior to WEF, presumably with current government insiders.

What additional “temple calculations” do institutional investors still have to make that must remain structurally exposed to some degree of MSCI ACWI-exUSA?

GCC and MSCI Israel Proxy ETFs Provided Institutional Investors Liquidity, Optionality, Liquidity, and Beta Management Strategies During the Shocking Events of Week One of the War of US vs IRGC.

At $.15 Trillion in combined Market Cap, GCC states (plus NATO ally, MSCI Turkey) and Israel (Israel’s equity market is in MSCI DM) are just too big to ignore within MSCI ACWI-exUSA, especially for investors seeking to reduce commodity sensitive MSCI Asia Index exposure, or hedge nat gas risk to mainland Europe.

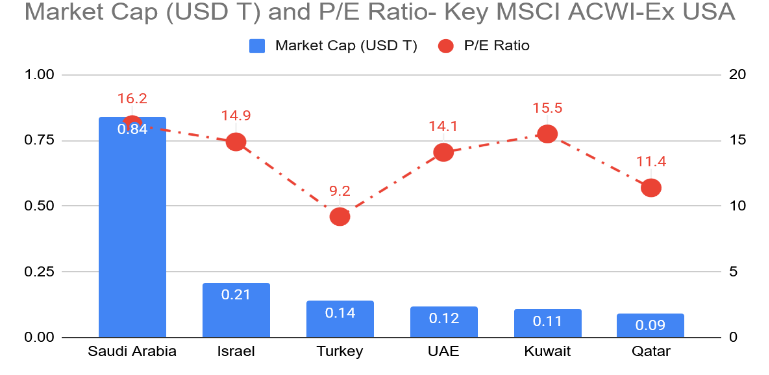

Too Big to Ignore: GCC States & Israel such as KSA and UAE have much lower P/Es than broader MSCI ACWX-USA (~19X)

Source: MSCI, Google Gemini as of 2/28/2026

2. Update on DuLac Capital Advisory’s EIS/KSA Barbell Strategy Institutional Implementation Prediction:

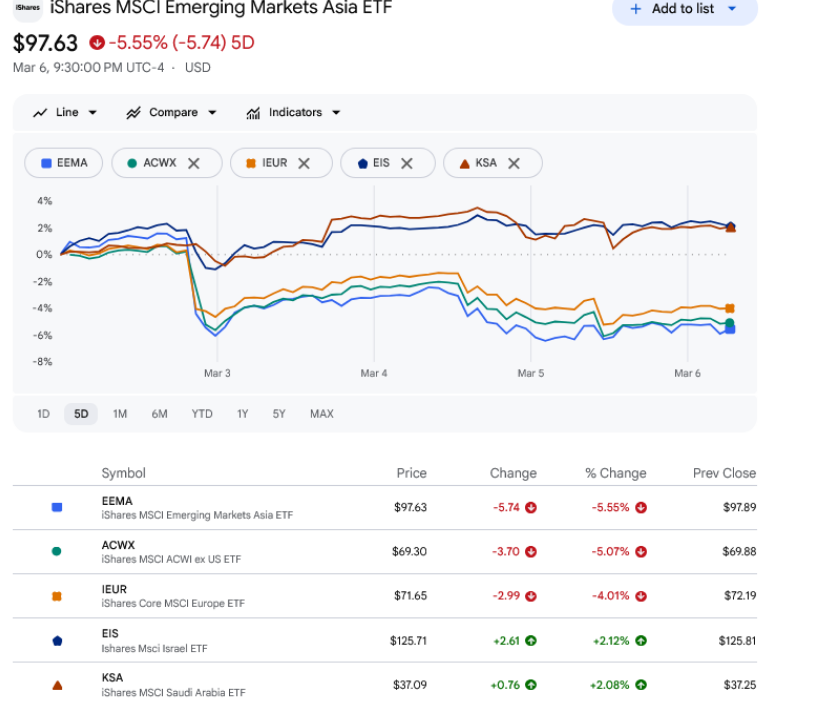

Meanwhile, following the war’s outbreak last Saturday (3/2/2026) as DuLac Capital Advisory L.L.C. projected on 3/2/2026 that many institutional investors hedged their commodity sensitive MSCI EM Asia (e.g., iShares MSCI EM Asia ETF: EEMA ) by incorporating various barbell strategies with the most liquid beta instruments for both MSCI Israel: e.g.,iShares MSCI Israel capped IMI ETF: EIS. And MSCI Kingdom of Saudi Arabia (capped IMI): e.g, iShares MSCI Saudi Arabia ETF: KSA.

This approach delivered strong risk adjusted returns from Monday-Friday relative to both MSCI EEMA and even MSCI ACWx-USA (e.g. ACWX ETF).

Source: Google Finance, iShares.com as of 3/7/2026

3. New Phase for “Temple Calculations”:

I now believe we are approaching a new phase for the institutional investors to consider due to the black swan event of the closure of the Strait of Hormuz– even though it hurts the IRGC’s main source of revenue– and the IRGC targeting of industrial-energy-tech infrastructure in many of the GCC states, such as the data center in UAE.

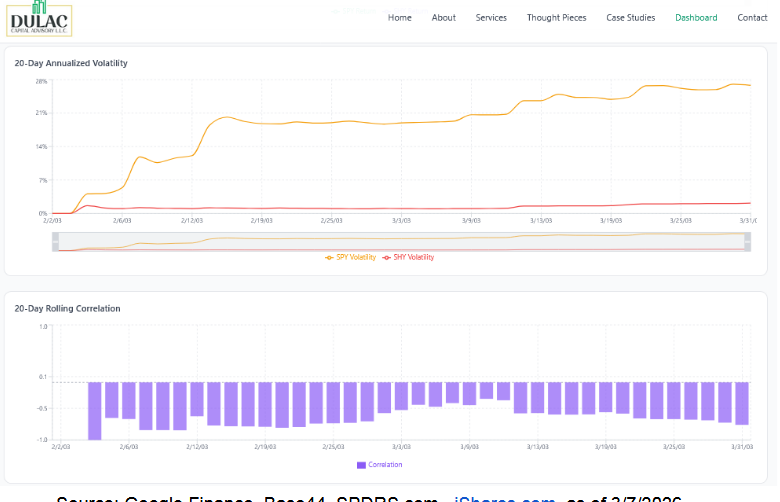

Trader Muscle Memory or Muscle Spams– Historical Precedents: 1990, 2003, and 2022:

The rise in vega risk and increased correlations across many commodity sensitive regions to an 80/20 portfolio portends that many institutional investors may go back to muscle memory of not just 2022, but also 2003, and even 1990– when President Saddam Hussein targeted Kuwait’s energy infrastructure in his razed earth retreat campaign.

There is rising correlation between MSCI Asia and the broader market as measured by iShares Aggressive Portfolio ETF AOA (80/20 Stocks-bonds).

This rising correlation though is coming with rising volatility and lower expectation of returns: not a good recipe for portfolio utility.

In comparison, as projected, KSA and EIS have both held up well in the turmoil on a relative basis and still have lower correlations vs AOA than commodity shock sensitive EEMA or MSCI Europe (e.g., iShares ETF: IEUR).

Source: Google Finance, Base44, iShares.com as of 3/7/2026

This could lead to institutional investors maintaining a higher risk exposure to the GCC states plus Israel– which comprise about $1.5 Trillion out of MSCI ACWIxUSA’s $40 Trillion in market cap– vs MSCI EM Asia or even MSCI Europe.

The risk though could be that with Qatar’s force majeure announcement, there could be a strain placed on their financial services companies that lend to the commodity producers; force majeure actions could expand to other hard hit GCC states such as UAE and even Kuwait.

This could especially be the case given the bombardment of Shaheed drones and IRGC missiles that is occurring around the clock. According to Joe Lindsley of Under Fire News,who covers drone warfare in Ukraine and Mideast, “the US is using $2 million missiles to shoot down $10,000 [IRGC] drones.” Most institutional investors did not fathom aspects of the Ukraine war coming to GCC states, despite news reports since 2022 that Russia Federation was mass procuring the IRGC’s shaheed drone.

This changes the calculus on more outright bullish aspects in the near term for GCC+Israel exposure– but not on a long term basis given technology tilt, growing clarity in their financial systems, and growth projects such as Vision 2030, buttressed by the prospects of the expansion of the Abraham Accords.

Thus, in the near term, institutional investors may sell upside calls on their preferred MSCI EM positions in the GCC, plus options on underling stocks that comprise MSCI Israel IMI (capped), while buying protection for their MSCI EM-ex GCC positions which are still up on a trailing one year basis.

Institutional Investors that barbelled existing long positions on MSCI Israel via EIS and MSCI Saudi Arabia via KSA ETFs outperformed MSCI ACWI-exUSA and MSCI EM on an absolute and especially a risk adjusted basis. 20D Trailing Annualized Volatility for KSA actually undershot the uptick experienced by ACWX– much due to the large Asian exposure in the broad index (that excludes USA).

Source: Google Finance, Base44, iShares.com as of 3/7/2026

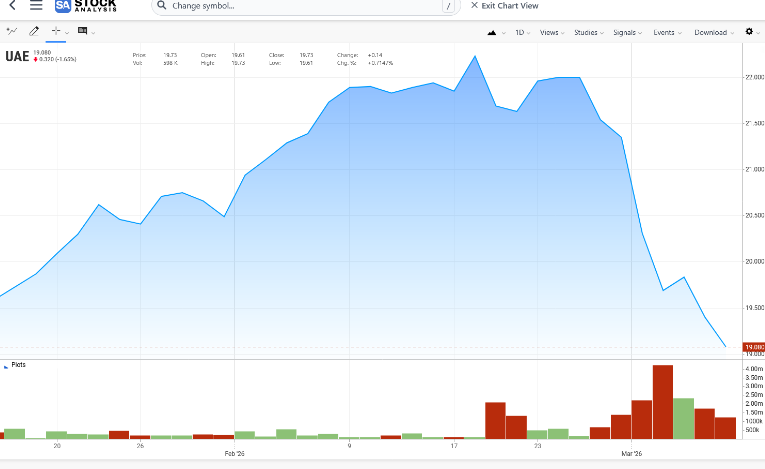

4. ETF Resilience: UAE Liquidity Acts as a Vital Volatility Buffer Amid Regional Market Closures:

Despite the UAE equity market closure on Monday-Tuesday this past week, iShares MSCI UAE ETF (UAE) continued to trade– providing institutional investors liquidity, beta management, cash drag mitigation, and collateralized security lending (the ETF and underlying) benefits during the turmoil.

UAE has been a growing constituent of MSCI EM– comprising nearly a similar share as traditional EM heavy weight, MSCI Turkey (TUR) over the last year.

Despite the underlying market being closed in UAE due to IRGC missiles and drones attacking its industrial and hospitality centers, over 4 Million shares traded on Monday 3/3/2026 in the US listed ETF: vs ~114K avg per NASDAQ.

Thereby proving an institutional use case study in ETF beta management during vol convexity spikes.

Source: https://stockanalysis.com/chart/UAE/ as of 3/7/2026

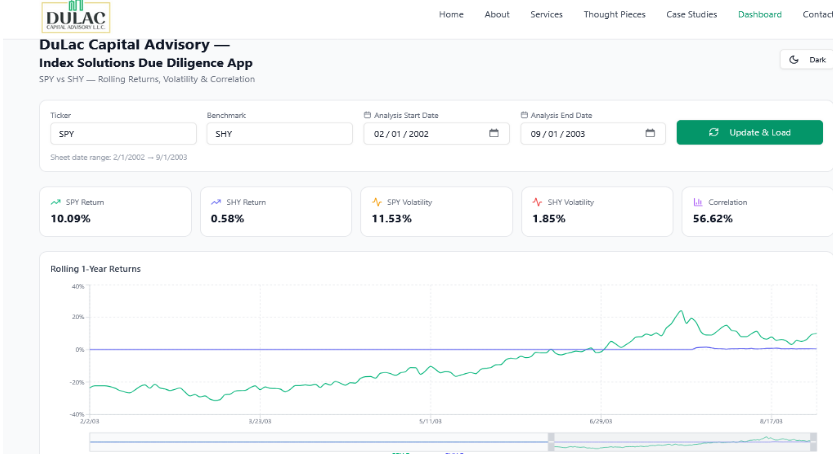

Saddam Hussein’s attacks on Kuwait’s Energy Structure in 1990– and what it did to the markets, economy, and consumer psychology. The oil shock led to a gasoline price spike, which soured consumer sentiment and led to a slow down in spending– especially given Dr. Greenspan at the time maintained a fairly restricted monetary policy. This ended up spelling disaster for the war hero President at the voting booth a year later. As Carvell famously quipped “It’s the economy, stupid.” Perhaps IRGC is planning on that scenario as well.

Twelve years later, when the victor President George HW Bush’s son took on Saddam’s Baathist regime once again, but this time to “finish the job”-- volatility in the S&P 500 jumped 5.5X to 24% from the period of early 1 February 2003 to 1st April 2003– muscle memory caused institutional investors to have concern again about oil supply chain shocks as Saddam’s scud missiles 2.0.

Source: Google Finance, Base44, SPDRS.com , iShares.com as of 3/7/2026

Those fears ended up not panning out though– after a steep 31% linear price decline by the start of the war, the index, and its most liquid ETF, SPY from SPDRS, rallied by mid summer to positive returns for the year. Thus enabling investors who were structurally long the index as a core portfolio risk, to monetize the volatility via collars, covered calls, security lending for income generation, and other option strategies.

Source: Google Finance, Base44, SPDRS.com , iShares.com as of 3/7/2026

5. “The Unknown Unknowns”:

The late Princeton wrestling champ and Secretary of Defense, Donald Rumsfeld, described the difficulty of dealing with the Baathist and Al Qaeda insurgency in Iraq with insight on vega risk: the unknown unknowns.

Risk of UK Leaving US Hanging for a Suez 2.0 Scenario: UK PM Sir Keir Starmer imitates President Ike– pulling a Suez Canal Crisis 2.0 scenario out of far fetched to a necessary risk management for institutional investors– this adds to not just the downside convexity risk for the market, but also uncertainty over whether traditional risk havens such as DM government bonds can act as a ballast to the equity market uncertainty.

Why? Traditional allies aren’t working together: this doesn’t portend well for a “few week conflict”, nor for any sign post that the feared commodity shock may subside with the Five Eyes working well as a team. For instance, recently BP had to evacuate its British workers from its oil field work in northern Iraq.

The UK (e.g., iShares MSCI UK ETF: EWU and Franklin FTSE United Kingdom ETF: FLGB) has placed constraints on its oldest ally, the USA, in terms of forward use of UK bases; this is interpreted by the market as a factor that could prolong the war and thus further drive up commodity shock risk.

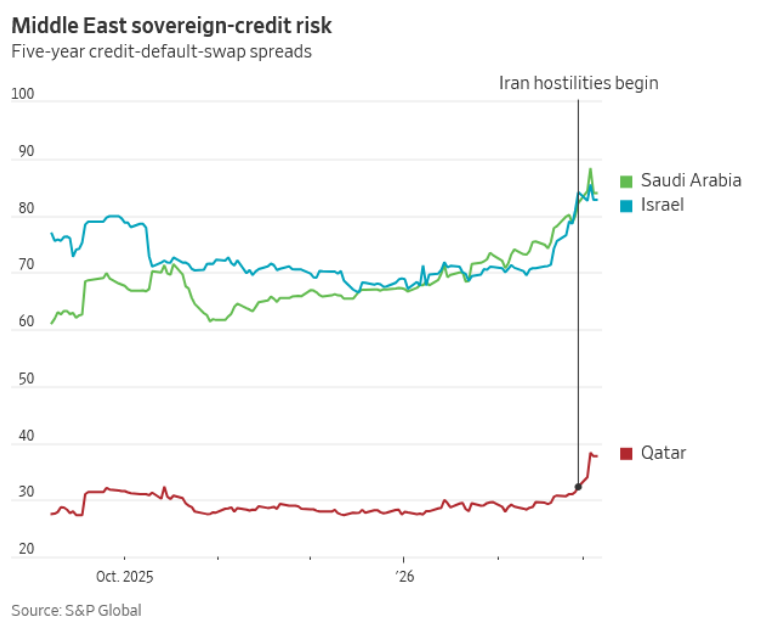

This is a key reason why DM sovereign bonds sold off– and, per the WSJ, GCC sovereign risk as measured by CDS increased as well this past week. In 2022, there was nowhere to hide except for commodities, this trade scenario could be even worse given the massive reliance on GCC hydrocarbons by the DM-ex USA and the EM world.

Below is a chart from the WSJ regarding the uptick in sovereign bond CDS for Kingdom of Saudi Arabia, Qatar, UAE, and Israel– don’t be surprised if the Trump Administration announces a “Brady Bond Redux” to help offset sovereign risk for its key Mideast allies.

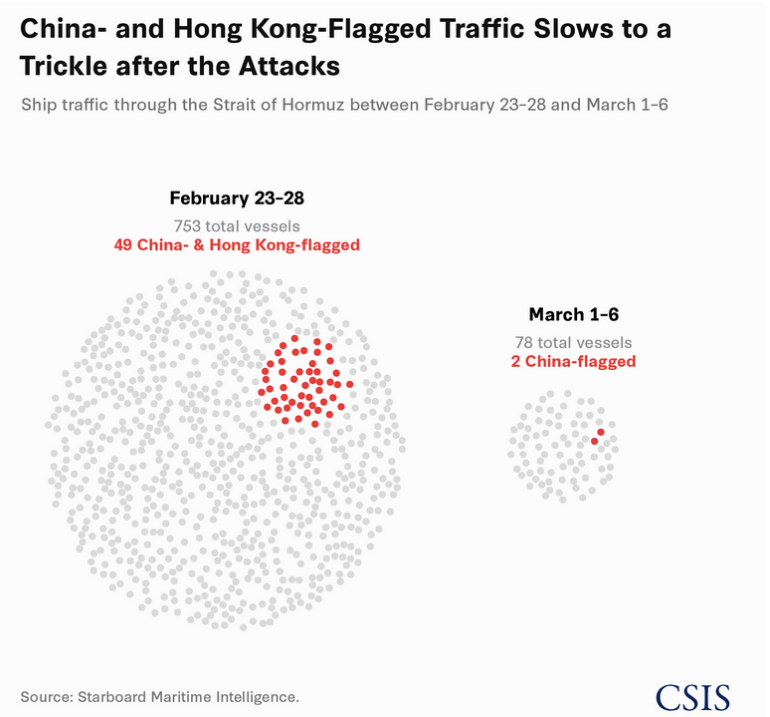

“The unknown unknown” now is a factor of how long the Strait of Hormuz will remained closed to to IRGC targeting and what the second and third order impacts will be on PRC ties to the global economy. Thus, institutional investors may very well have to plan for the probability that this time may be much different than 2003. As CSIS has cogently described the unthinkable just eight months ago– the IRGC has closed the Strait of Hormuz where even its key client state, People’s Republic of China has had difficulty getting its flagged LNG/Oil vessels through. The CSIS points out that the IRGC has been targeting ships in the Strait of Hormuz– contributing to over a 90% decline in PRC and Hong Kong Flagged ships getting through. This signals to the world that the PRC’s massive economy may be experiencing a commodity shock soon, and its lofty foreign investment may then begin to slow down vs. expectations prior to the war.

Soure: CSIS as of 3/7/2026

Additionally, the Middle East Forum has pointed out that approximately 31% of the sea borne oil is shipped through the Strait of Hormuz, and the WSJ indicates 20% of LNG is exported through there as well. The People’s Republic of China (e.g., iShares MSCI China All Shares ETF: MCHI) is the top buyer with over 4 out of its 11 Mbd of oil imported from the Persian Gulf countries– a quarter of that is from Iranian crude– all passing through the Hormuz Strait. India (iShares MSCI India ETF: INDA) is “even more dependent on Middle Eastern energy than China.”

Also, 7 percent of the European Union’s oil imports come from KSA. Qatar has a 10 percent share of the European LNG market per the Middle East Forum. The Middle East Forum pointed out the USA’s recent expansion into LNG export ties to Europe, which could serve as a ballast vs the more worst case scenarios in Asia.

Additionally, much to the chagrin of those that were seeking investment safe havens for the 21st century in the GCC– in addition to industrial and tech supply chain infrastructure of the GCC member states hosting American Troops. Much of which, the PRC has heavily invested in— However, MCHI could catch a bid relative to MSCI ACWI if signs of the Strait of Hormuz opens up or if more oil deals with Venezuela are allowed by the Trump Administration.

MCHI Correlation has increased with AOA: and risk adjusted return Trends have Deteriorated– This doesn’t Bode Well for Portfolio Utility until Signs of Easing of fthe Closure of the Strait of Hormuz Emerge

Source: Google Finance, Base44, SPDRS.com , iShares.com as of 3/7/2026

6. Summary– Three Key Takeaways for Capital Allocators:

Fiduciary Imperatives

Supply Chain Strain: U.S. military confrontation with Iran is depleting Patriot missile interceptor (e.g., iShares Aerospace and Defense ETF: ITA) supply production constraint risks as pointed out by the WSJ last week– this could thereby weaken perception of strong air defenses for the GCC, therefore raising their capital market’s WAAC.

Asymmetric Hedging: EIS/KSA barbell approach allowed investors last week to outperform MSCI EM Asia and MSCI Europe as the pair provided a combination of tech and modestly impacted energy-industrial exposure. The easy absolute return gains are likely in the review view mirror on an absolute basis. However, the pair may still continue to outperform on a risk adjusted basis– continuing to grow as a greater weight in MSCI ACWIxUSA due to commodity shock concerns.

Data Validation: With Qatar declaring force majeure, CIO teams must ensure AI-assisted research isn't missing these rapidly evolving "black swan" signals. DuLac Capital Advisory L.L.C. recommends that institutional investors still use Bloomberg PORT and SPLC functions or Factset API for revenue contribution screening inquiries.

DuLac Capital Advisory L.L.C. specializes in tech-enabled investment due diligence and portfolio efficiency consulting for institutions. If there's interest in deeper validation, scenario modeling, or bespoke product due diligence on related ETF/index strategies (e.g., stress-testing barbell allocations under prolonged energy disruptions), we’ll be happy to facilitate an introductory discussion with their team to explore potential collaboration.

DuLac Capital Advisory’s ETF/Beta Solutions Risk Due Diligence App : https://www.dulaccapitaladvisory.com/services

(sample version for institutional investors only)

Contact

DuLac Capital Advisory—Independent index solutions due diligence for asymmetric event risk.

ryanScott@dulaccapitaladvisory.com | +1‑516‑838‑6833

Investment News, Market Insight, and Investment Insight Disclaimer

The information, investment news, and policy insights provided by DuLac Capital Advisory L.L.C. ("the Firm") through its publications, reports, newsletters, and communications, including but not limited to Investment News, Market Insight, and Investment Insight, are intended for informational and educational purposes only. These materials are not to be construed as specific investment recommendations or advice. DuLac Capital Advisory L.L.C. is a technical services management consultant for companies and institutional investors. DuLac Capital Advisory L.L.C. does not receive any revenue from any company or service mentioned in this insight piece.

Not Investment Advice:

The materials provided by the Firm do not constitute investment advice or recommendations to buy, sell, or hold any securities or investment products. The insights offered are general in nature and do not take into account the individual circumstances, investment objectives, risk tolerance, or financial situation of any particular institutional investor or recipient.

No Reliance:

Institutional investors should not rely solely on the information provided by the Firm for making investment decisions. It is recommended that investors conduct their own due diligence, seek advice from qualified financial professionals, and carefully consider their investment objectives and risk appetite before making any investment decisions.

No Guarantee:

While the Firm strives to provide accurate and up-to-date information, there is no guarantee of the accuracy, completeness, or reliability of the information provided. The financial markets and economic conditions are subject to change, and the information provided may become outdated or irrelevant over time.

Risk Disclosure:

Investing in financial markets involves inherent risks, and the value of investments may go up or down. Past performance is not indicative of future results. Institutional investors should be aware of the potential risks associated with investment decisions and should consult with professionals who are qualified to provide personalized investment advice.

No Endorsement:

Any mention of specific securities, investment products, or companies does not constitute an endorsement, recommendation, or promotion of those securities, products, or companies by the Firm. The inclusion of any such information is for informational purposes only. No compensation was received from including any investment product or technology into the White Paper.

Legal and Regulatory Considerations:

Institutional investors are responsible for understanding and complying with all applicable laws, regulations, and guidelines related to their investment activities. The Firm's materials are not intended to replace or substitute for legal or regulatory advice.

The Firm disclaims any liability for the use or interpretation of the information provided in its materials. Institutional investors should use their judgment and exercise caution when relying on any information provided by the Firm.

For personalized investment advice tailored to your individual circumstances, we strongly recommend consulting with licensed financial advisor at a major Wealth Manager.