Mutli-Factor Risk Reduction & Alpha Amplification via Tier 1, 2 Capital Securities Project

Case Study— Implementing Sector Rotation Strategies with ETFs for Strategic Tilts and Rapid Beta Exposure-

via a “Core-Satellite” Approach with Tier 1 & Tier 2 Capital Security Index Products and

Source: Bloomberg PORT, BlackRock Aladdin PRT. Past performance does not imply nor guarantee future results. This case study is for institutional investment managers only.

Client Challenge

Following a strong rally in fixed income rates and IG credit, an active Multi Asset Income Fund Manager viewed Tier 1 and 2 preferred stock and hybrid credit as an asset class that could provide attractive relative value to senior secured credit and dividend equity.

The PM team viewed preferred/hybrid Tier 1, 2 capital as a pro-cyclical complement to their existing fixed rate IG credit exposure.

Due to heavy inflows to their fund, the client found it challenging to achieve enough diversification and scale through single security selection.

Ryan Scott’s Analysis & Insight

The client asked DuLac Capital Advisory L.L.C. to analyze their existing multi-asset class portfolio utilizing BlackRock’s Aladdin and Bloomberg’s PORT for comparative purpose.

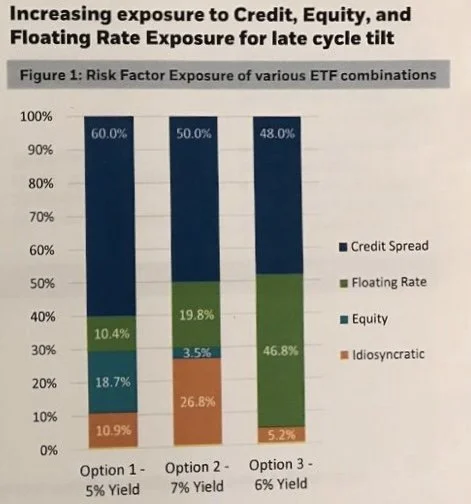

The client wanted to determine which index solutions could help boost exposure to three key pro-cyclical factor tilts:

Credit Spreads

Equity Earnings Yield Sensitivity

Floating Rate Sensitivity

A proposal was crafted with three index product options that would enable the Multi-Asset Income fund manager to increase the probability of gaining exposure to the above mentioned factor tilts, reduce total cost implementations, and increase positive idiosyncratic risk.

Solution: Core-Satellite Approach

The client decided to implement their target exposure through a combination of the cohort’s most liquid ETF that also had the highest floating rate exposure, and several OTC hybrid Tier 1—non Euro AT1—hybrid credit securities with call protection above the average.

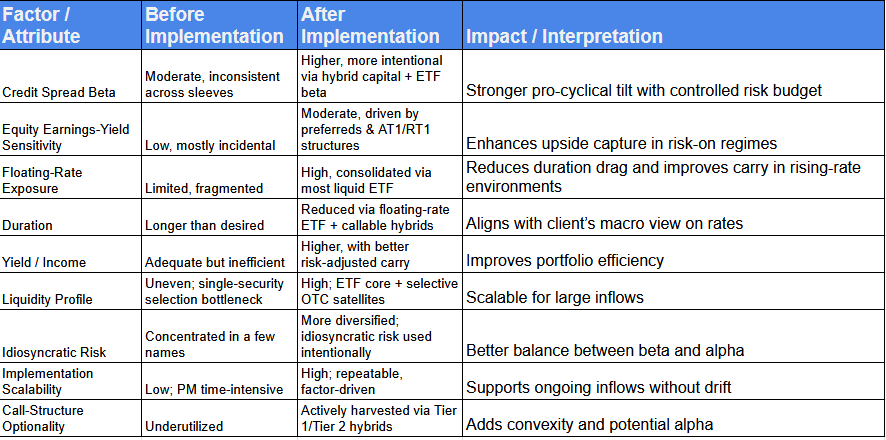

DuLac Capital Advisory L.L.C. Before/After Tier 1, and T2 Hybrid Credit Factor Exposure Insight