Crouching “DEIger” Hidden ESG Dragon: is ‘Collectivist Stakeholder Capitalism’ the next Enron or Growth Engine?

The push back against the DEI & ESG in light of the Ivy League & MIT Presidents’ Capitol Hill debacle reveals a looming battle to dismantle “Stakeholder Capitalism” as the new Dogma of the Public Markets— and thus a template for other active investors to call options that will monetize a return back to orthodox Shareholder Capitalism.

In December 2023, American attention was drawn to the Capitol Hill hearing on Combating Antisemitism at Universities hosted by the House Workforce Committee. The three credentialed Presidents of Harvard, MIT, and University of Pennsylvania could not answer a simple Yes or No question about whether “calls for genocide by students on campus”— was not only illegal in the USA, but also penalties on their campuses per University policies.

Given none of three Presidents had a track record of explicit bigotry, it does not appear that their reprehensible equivocation was driven by classic Antisemitism. Additionally, their bogus “context dependent” non-answers were not due to lack of intelligence or access to information about the history of the Pogroms and Holocaust against people of Jewish heritage.

DuLac Capital Advisory L.L.C. posits that indifference and moral impotence are problems stemming from the anchoring effects of the rise of “Stakeholder Capitalism” based management strategy. This Thought Piece covers the implications to investors, policymakers, and industry on the rise of the Stakeholder Capitalism model within the Anglo-America sphere, which has traditionally incorporated more of a Shareholder Capitalist approach to markets and government involvement.

This is important since both public and private actors have designated trillions to various so called “ESG-DEI” aligned Sustainable investment and policy mandates in both public and private markets. The net present value total may amount to more than what was invested in the Industrial Revolution (source: Katie Koch, former head of GSAM Public Equities in October 2021 interview in “ICE House” podcast).

If that historic amount of capital is allocated to operations over-anchored by “context dependent Stakeholders”, then profitability and jobs will become indeed very dependent on taxpayer or shareholder largesse. Therefore, could Stakeholder Capitalism be inadvertently falling into the trap of the “Road to Serfdom” that Dr. F.A. Hayek warned about during the Cold War? If so, there may be an under-appreciated downside “stakeholder Lethargy Risk Factor” that must be now weighed by fiduciaries from both an investment policy standpoint: as productivity and a civil shareholder litigation risks may soon manifest in these Stakeholder Capitalist Ecosystems.

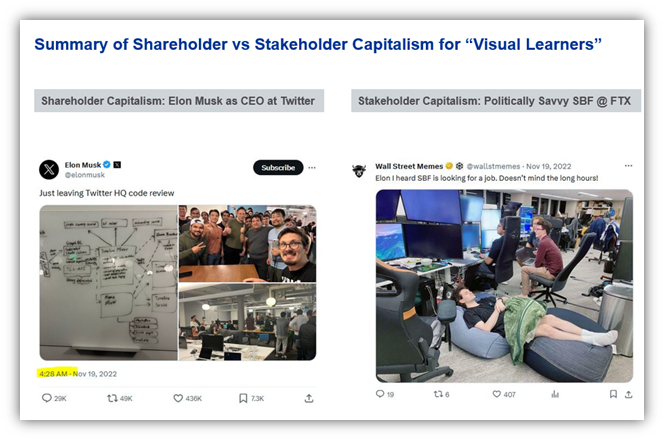

For visual learners, that are short on time, below is a rough approximation of the difference between Shareholder Capitalism and Stakeholder Capitalism. It’s important to recognize the difference—especially since trillions are at “stake” given the massive asset over the last 15 years since the Global Financial Crisis and subsequent proliferation of UN Climate SDG and COP28 Mandates.

Shareholder Capitalism creates a positive environment for innovation and hard work as long as proper Governance rules are in place that align with constitutionally sound laws of the State.

Executive Summary:

2023 began with the rise of backlash against ESG, with Elon Musk even calling it “Rebranded Communism”, as explained by Matthew Mohlman of Monument Ventures. This push back dovetails with the more recent backlash against DEI capital allocations in industry, investment portfolio mandates, and government policies. Laura Brady, Strive Asset Management, explained in a December Thought Piece that even though corporations are no longer discussing “DEI” and “ESG” at publicly recorded conferences, they still have significant capital allocated to it via workforce mandates— and most S&P 1500 companies still highlight the concepts on their websites.

DuLac Capital Advisory L.L.C. has found evidence that public market ESG-DEI capital expenditures and investing mandates are more likely used as an attempt to increase “Goodwill as an Asset” on the balance sheets of Companies (aka, “Brand Value”), rather than produce tangible results to both shareholders and the “communities” (environmental and social) as pledged in corporate marketing documents.

DuLac Capital Advisory L.L.C. research into the relationship between DEI and ESG indicates they are both entrenched within the recently prominent “Stakeholder Capitalism” ecosystem. Therefore, the bigger picture is whether Stakeholder Capitalism really should be regarded as a rightful successor to Dr. Milton Friedman style Shareholder Capitalism— the latter proved to be the best model to win the Cold War, after all. However, since Mainland China is a major supporter of “Sustainable Investing”, within “Socialist Chinese Characteristics,” then a prudent investor must weigh their claim against the assets less debt held within the Stakeholder Capitalism ecosystem.

For ESG and DEI to survive as a going-concern within the public markets (regardless of whether it’s “rebranded” in America per the 01/10/2022 Wall Street Journal article), the two capital mandates must be accounted for on corporate balance sheets, or be moved to charitable allocation via the company’s philanthropic foundation divisions. As supporters of the former Presidents of U-Penn and Harvard have found out: just because one is a vocal “Harvard Stakeholder” on a MSNBC tv show, does not mean their stake will outweigh the authority and power to enact change that actual share of capital provides. Private Equity impresarios, Marc Rowan and Bill Ackman efforts demonstrated that Shareholder Capitalism is back in America.

No ‘rebranding’ or ‘re-framing’ will help assuage risks until investors better understand the answer of these three fundamental questions at stake:

The People’s Republic of China has long implemented a version of Stakeholder Capitalism over Shareholder Capitalism; how has its market performed over the “long term” vs. more Shareholder Capitalist markets?

On average, within the public markets, companies that operate in countries that tend to favor a more Shareholder Capitalist approach, seem to outperform companies that operate in countries that incorporate a more of a Stakeholder Capitalist model.

If Stakeholder Capitalism is real and tangible, why are corporations and investment firms reticent to explain the cost accounting for all of their “stakeholders” on their GAAP aligned and independently audited Balance Sheet, Cash Flow statement, and Income Statements?

Since ESG and DEI are major initiatives within the public market space of Sustainable Investing, there is increased risk to balance sheet impairment and unrecognized civil legal claims if the corporate ESG-DEI goals marketed, are not actually accounted for within the GAAP framework for Financial Statements for publicly registered companies.

In a book that captures all of Warren Buffet’s Letters to Investors over a three decade period, Essays of Warren Buffet, the term “stakeholder” is never mentioned as a concept. The terms “share”, “shareholder”, and “shares” are mentioned over 500 times. How then could “stakeholder capitalism” be a true investment framework if the greatest public markets investor never thought it merit worthy in over three plus decades of investing?

Since the Stakeholder Capitalist Model may be more aligned with the Mainland China economic sphere of influence, does it produce merit worthy returns in the private markets—and thus the novel concepts interest from major Western Investment Companies and Industry?

Mainland China has been governed by a Marxist and authoritarian government since the 1950s. As previously demonstrated, its public markets have likely been penalized by the heavy hand of the Government’s involvement within the publicly traded companies’ operations.

However, the Stakeholder Capitalism model may have benefits from a private market standpoint: this could especially be true where capital and labor intensive investments that require government approval in any nation, such as “Sustainable Infrastructure”.

Crouching “DEIger”, Hidden “ESG Stakeholder Dragon”

Just as too much data in the consulting or industry can lead to “analysis paralysis”, can too many stakeholders with unrecognized claims to firm capital lead to “executive paralysis” by key decision makers under game-time decisions? Apparently they, and especially Ms. Magill and Dr. Claudine Gay’s backers in the media (see NY Times Opinion piece from a pro Dr. Gay writer, Dr. Cottom that dubiously assert “merit has no definition” for example) were surprised to find out that the impact of Share owners of the invested Capital—such as Mr. Marc Rowan of Apollo Global and Mr. Bill Ackman of Pershing Square—actually does matter to enact change in an organization. In effect, the silver dollar outweighs the squeaky wheel when it comes down to bottom line decisions of institutions that seek sustainable profit.

The three Presidents inability to provide a decisive answer to an interview question that any high school senior could answer in a college interview, indicated that they mistakenly fell into the confirmation bias trap of the Squeaky Wheel Stakeholder model. Firms such as Goldman Sachs, JP Morgan, and Google all announced close to $1 Trillion in capital allocation designated to ESG and DEI oriented strategies between 2020-2021.

Are these global Fortune 1000 firms also then at risk to operational efficiency, and thus profitability, driven by indecision caused by an over reliance on the false sense of security of the recently popular theory that “Stakeholder Capitalism” for collective social good trumps shareholder rights based capitalism? Yes, they are. Additionally, there are civil legal risks at stake as well that may peak activist shareholder capitalist oriented investors, and should awaken passive “Stakeholder Capitalist” collectivist investors.

DuLac Capital Advisory L.L.C. also believes many of the companies touting ESG-DEI capital allocation mandates since 2019 as a solution to “improve communities” and “boost long term shareholder profits” may perhaps be doing so to signal a path to a competitive advantage via “ESG-DEI Moats”, however, if so, they must account for it within the GAAP framework. In the end, Free and open market capitalism requires accounting standards that have transparency to all potential investors. If one cannot map on the balance sheet how X Billion in capital designated to “DEI” investments, actually improved the asset profile, raised Cash from Operations or Financing, and elevated Operating Margins, then that company—whether investment or industry—will be at increased risk of civil shareholder liability suits and State based civil suits as well: Tennessee is the most recent example.

However, within the capital non-intensive private market tech sector, such as OpenAI, SpaceX, Anthropic, and Mistral show that investors really do not care about “Diversity” or “Environmental” factors as constraints on capital allocation within high growth industries that require extremely high intellectual productivity with the lowest number of people in order to break even on ROIC.

At the end of the day, investors, industry leaders, and policymakers should always pause and ask the question: What would Warren Buffet think about “Stakeholder Capitalism”? His lessons over the last 60+ years, rooted in Dr. Benjamin Graham’s value investing, boil down to conservative accounting practices as paramount. Therefore, DuLac Capital Advisory L.L.C. urges all “stakeholders” to pause and ask:

Whether public or privately held via VC/PE, what are the purported “ESG-DEI” capital mandate’s (GAAP accounting eligible) ROIC for shareholders since trillions of ESG mandates have been launched under the shade of the “Stakeholder Capitalism Tree”?

Whether public or privately held via VC/PE, what has been the net debt and net tax revenue impact for “public private partnership” projects seeking to promote sustainability?

Heightened Risk of Shareholder rights civil lawsuits from both the “left” and the “right” that due to the Lack of Financial Statement Disclosure Transparency—

DuLac Capital Advisory L.L.C. believes that professional investors, industry, and policymakers may be under-appreciating the risk that Stakeholder Capitalism companies face in light of potential rise of “Failure to Perform” and potential Antitrust oriented “shareholder rights” civil lawsuits from both the “left” and the “right” political actors. Stakeholder Capitalism within the private markets (PE, VC) sphere that involves goals such as capital intensive “Sustainable Infrastructure” investing and job creation, may actually have merit: especially since the build out of nations such as the UAE and Mainland China have corresponded with more Stakeholder capitalist strategies.

Therefore, just as pro Net Zero CO2 transition “stakeholders” are transitioning their verbiage away from ESG (A Progressive’s Case for Getting Rid of ‘ESG’ by Dr. Alex Edmonds of LSE, WSJ August 19, 2023) to “Corporate Social Responsibility”, the actual verbiage of “DEI” will likely also be rebranded to something else, such as “Civil Rights Act Compliance” (source: Dr. Alvin Tillery of Northwestern University and CEO 2040 Strategy Group, a civil rights consulting firm for Corporates).

This echoes Elon Musk’s recent forum with Italian policymakers in December 2023 where he stressed that Oil and other higher intensity carbon energy products are still needed in the “short and medium term.” He also declared that much of the doomsday announcements of climate change as overblown: noting that it is not an “risk to Civilization”— a challenge, yes, not one that is existential. His words are important as he is an actual practitioner, and thus prudent active investors will use his insight as a key data input to update their models: perhaps identifying room for taking the “other side of the trade” on ESG-DEI, and in particular in the context of public markets recent dogma shift to “Stakeholder Capitalism.”

Nonetheless, since “ESG” and “DEI” are branches of the “tree” of Stakeholder Capitalism, and since major publicly traded corporate executives have stated Stakeholder Capitalism is beneficial for shareholder’s long term value, there is an under-priced risk of shareholder rights and State AG based class action lawsuits for mismarketing, failure to perform/deliver, accounting irregularities, and even Antitrust legal litigation that is yet to be recognized by promoters of Sustainability factors within public market investments.

However, capital intensive private market investing such as “Sustainable Infrastructure investing”, will likely still underscore various forms of ESG-DEI factors as a positive for their LPs: especially since Mainland China, the hidden “Stakeholder Dragon,” has been a key long-time supporter of the concept of Stakeholder Capitalism to achieve their view of “harmonious social goals.”

The issue for the public stock and bond markets to realize is that there will likely be increased momentum of negative perception regarding "ESG-DEI" capital mandates. This decline of popularity may be buttressed by actual examples of sub-optimal investment returns ex inflation/government spend. This declining perception of the value of “ESG-DEI” capacity to produce competitive profit, may thus end up mapping to the intangible Goodwill as an Asset; may soon need to be partially converted to a liability side of the Balance Sheet as consumer sentiment, investor shareholder rights lawsuits, and State Government action demands more transparency. This will be the case even if companies may be slow to recognize it on their financial statements.

Therefore, even if DEI-ESG survives within the private market space, as its crouches within the overall “Dragon” of Stakeholder Capitalism for private market strategies with Mainland China at the table, the collectivist concept of “Stakeholder Capitalism” as a positive framework for public company ecosystem in the Anglo-America sphere, may end up becoming the ”next Enron”—a major short that could unlock value for active investors seeking to “liberate” artificially trapped/impaired assets-- of the 2020s.

Ironically, examining “Dragon Shares” (Chinese based companies that list ADRS on NYSE, NASDAQ, or LSE), provides a n interesting proxy to illustrate the challenges that over-reliance on the Stakeholder Capitalism model may face against the upcoming awakening of Shareholder Capitalism Redux.

Stakeholder Capitalism for social good is touted as beneficial in the “long term” for shareholders and society. However, Dr. Keynes, when he was trying to rid England, America, and France from its fixation to the Gold Standard, he cautioned about the religion of “long-termism” as a sort of excuse that disables action in the here and now: “In the long-term, we are all dead.” (Source: Lords of Finance by Liaquat Ahamed). Therefore, for reality’s sake, this analysis will view medium term as 3-5 years, and long-term as 5-10 years. Beyond that, is largely a non-sequitur within the Anglo-American economic sphere of historical support for free enterprise.

Comparison—Stakeholder Capitalism vs Shareholder Capitalism: PRC vs USA in the Year of the Dragon

Stakeholder Capitalism for social good is touted as beneficial in the “long term” for shareholders and society. However, Dr. Keynes, when he was trying to rid England, America, and France from its fixation to the Gold Standard, he cautioned about the religion of “long-termism” as a sort of excuse that disables action in the here and now: “In the long-term, we are all dead.” (Source: Lords of Finance). Therefore, for reality purpose medium term will be viewed as 3-5 years, and long-term as 5-10 years. Beyond that, is largely a non-sequitur within the Anglo-American economic sphere of historical support the free enterprise model.

The statements and marketing documents on major S&P 1500 companies in support of “Stakeholder Capitalism” to achieve allegedly profitable social and environmental goals (DEI and ESG screened), must back up those claims with bottom line accounting that meet GAAP standards. Institutional investors that have tried to map claims of the tangible collective benefits of Stakeholder Capitalism back to GAAP compliant accounting standards for publicly traded companies have often found it to be rather difficult.

The following two case studies illustrate that Stakeholder Capitalism oriented countries may be contributing to under-performing public stock markets compared to more traditional Shareholder Capitalism based countries. This means public stock and bond investors should be very wary of Western CEOs that tout the alleged profitable Shareholder Value that “Stakeholder Capitalism” provides over the medium or short term. Private markets may be a different story—especially in capital intensive infrastructure investing.

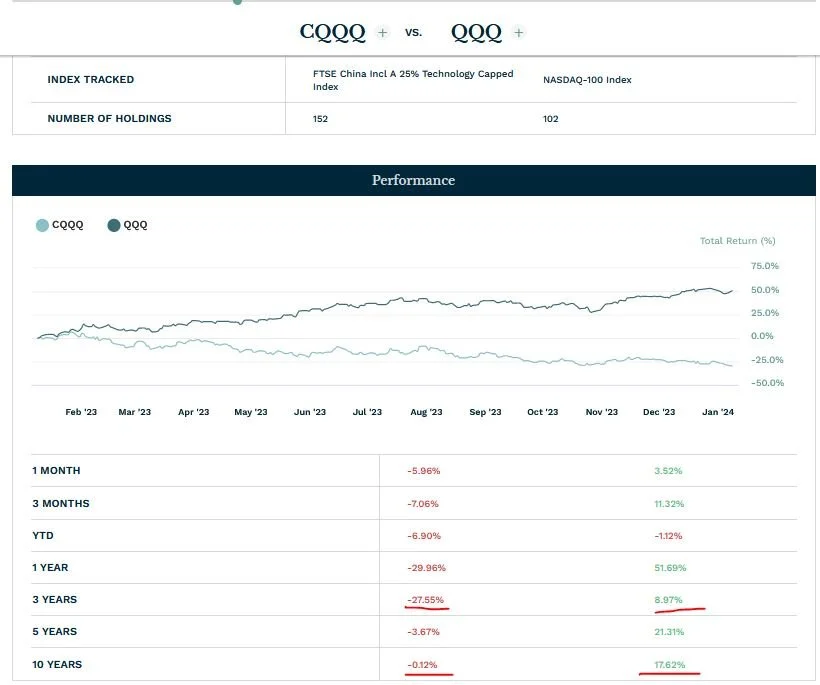

The chart below compares two ETFs with high growth factor due to heavy tech and consumer discretionary oriented exposure. The difference between companies that are forced to behave and operate within a collectivist "Stakeholder Capitalism" model of Mainland China, vs. companies that have historically had the liberty to operate within a "Shareholder Capitalist" market model of America.

Invesco China Technology ETF (CQQQ) vs. Invesco QQQ Trust (QQQ)

Source: ETF.com as of 1/11/2024 https://www.etf.com/etfanalytics/etf-comparison/EWT-vs-MCHI

DuLac Capital Advisory L.L.C. compared Stakeholder Capitalist Models vs Shareholder Capitalist Models to identify under appreciated risks and opportunities for active investors and policymakers to be aware of.

Long Shareholders, Short Freeloaders

The verdict is clear: there is a 17% long-term performance gap between Mainland China based tech-oriented companies vs. America’s more traditional model. Mainland China based, Beijing News Hour, and the Wall Street Journal, have long reported on the interests that the Mainland Chinese “authoritarian” government has placed on its private sector as a key “stakeholder” to ensure citizens of the People’s Republic of China receive the long-term value of the shareholder’s investment: the case of Ali Baba’s co-founder being sent to re-education wellness training after speaking out against President Xi is a clear example of the Government’s desire to achieve “harmonious” relations between all stakeholders.

This significant long-term performance differential between two tech-oriented ETFs, CQQQ and QQQ, underscore the potential “malpractice risk” that promoters of the social and environmental promises that Stakeholder Capitalism may face in the near future. Capitalism has lifted millions out of poverty worldwide over the last 150 years, and defeated communism and other collectivist models of America’s rivals during the Cold War. Yet, Stakeholder Capitalism, which is a type of collectivist central planning, has been touted as a keystone needed to “solve problems” of society.

Moreover, Ali Baba recently donated one of its Quantum Computers to a major STEM university in China as a token of appreciation. This may be par for the course for Stakeholder oriented Mainland China, but are Anglo and American passive 401k and pension investors aware of this when they allocate to Mainland China in a fairly passive manner via “diversified asset allocation strategies” with indexed based Open End Funds? Most likely not.

As there are always under-appreciated risk factors in the market (e.g., Enron, WorldCom, Lehman, FTX, First Republic Bank, etc.), this then points to opportunity for active investors to combine the historical benefits of active strategies. Specifically, there is an underpriced risk in the Stakeholder Capitalism camp of future campaigns—similar to what was utilized at Harvard/MIT—for active shareholder to exercise their rights to control a company’s capital allocation strategy by leveraging their shares to express contrarian stakes on how to better utilized underpriced assets of the company.

This strategy may be amplified through the use of shareholder rights based civil legal recourse and further accelerated through state based action in the spirit of Hamiltonian Federalism: the Tennessee lawsuit against a major Global Asset Manager filed in December 2023 may well be a harbinger of risk to come. Thus, Companies that have not “mapped back” the promised benefits of Stakeholder Capitalism to their GAAP financial statements, and that are underperforming the US broad market, may find themselves particularly vulnerable.

Stakeholder Capitalism for public markets may work for Mainland China, given its explicit Marxist constitution and Party, however, it is indeed a foreign concept in the Anglo-American investing world. The importation of that investment framework is certainly accruing heightened unrecognized risk of fiduciary based civil legal action led by State based policymakers and active investors.

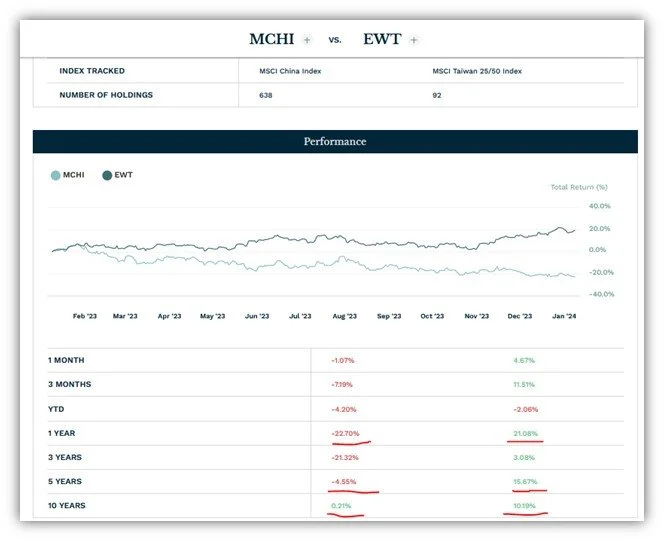

Case Study 2: Apples vs Apples: People’s Republic of China (Mainland China) vs Republic of China (Taiwan)

Below is a chart comparing the returns of highly traded ETFs from two countries of the same “ethnicity” (important for apples to apples), and even in the same geographic part of the world. Guess which one has long implemented Anti-Meritocratic based, and anti-metric focused mandates that are devoid of any historical tradition or observable and historically reality. Then guess which ETF is from a country which has been effectively "cancelled", despite its support for freedom of religion, speech, right to property, and innovation based capitalism:

Stakeholder based iShares MSCI China (MCHI) vs Shareholder oriented iShares MSCI Taiwan (EWT)

Source: ETF.com as of 1/11/2024 https://www.etf.com/etfanalytics/etf-comparison/EWT-vs-MCHI

The nearly 20% total return differential over the last five years, and ~10% differential over the last ten years reveals the risk for fiduciaries and US-UK based companies that market the benefits of “Stakeholder Capitalism” for long term benefits. In the end, Stakeholder Capitalism in the public markets may be rightfully viewed as another form of “Collectivist Capitalism”, which presents an opportunity for active investors to identify “big short” opportunities.

One nation (Republic of China—iShares MSCI Taiwan ETF: EWT) is an example of a “cancelled” country due to its reliance on Meritocracy: Republic of Taiwan has been effectively “cancelled” due to its success at defending constitutional liberty of religion, speech, property rights based on equal access to due process, and innovation capitalism—combined with the world order penalizing the nation for being “small” and thus not a great place to outsource tens of millions of Western Civilization’s manufacturing and tech jobs.

Meanwhile, the other ETF (iShares MSCI China ETF: MCHI) is comprised of companies from a country which has long been heralded as “America’s replacement” and celebrated for its “better model” of economic growth and government—even if at the expense of being able to freely go to Church, or Synagogue, let alone start one’s own business without having to sell a major “stake” to the Central Government.

Is the rush in the Anglo-American corporate world to adopt collectivist Mainland China like “Stakeholder Capitalism” like policies inadvertently “cancelling” good assets and proven methods to achieve operational efficiency and monetize innovation at public companies? Evidence is emerging that is indeed the case: therefore, expect an inflection point driven by active investors seeking to take the “other side of the trade” on Stakeholder Capitalism via old fashion shareholder rights arguments, that combine civil and legal action to compel public companies to not neglect its actual capital providers.

Hence, the chipping away at “DEI” by American investors, comes at a risk of also exposing that it’s the other side of the ESG coin: both are deeply embedded in the tree of “Stakeholder Capitalism” which is at the heart of the issue. Stakeholder Capitalism may very well be the model that Mainland China has agreed to permit within its Marxist vision of society, it however is not accretive to competitive profit driven investing in the Anglo-American sphere. Therefore, Shareholder rights focused investors that are skeptical of DEI and ESG claims must first look to the root of the problem: the emergence of Stakeholder Capitalism as “corporate dogma” within America and the United Kingdom.

Shareholder rights focused investors may increasingly view Public Company’s adoption of “Stakeholder Capitalism” as simply another type of Neo-Collectivism: Good for “Goodwill” credit with Governments and NGOs in the short term, but Detrimental to Shareholders in the long-term…..

Please add your contact information in the Message Box at the bottom of website to receive the rest of this White Paper. Thanks!

https://www.dulaccapitaladvisory.com

Ryan Scott

Executive Director and Founder

DuLac Capital Advisory

(+1) 516-939-6833

**Investment News, Market Insight, and Investment Insight Disclaimer**

The information, investment news, and policy insights provided by DuLac Capital Advisory L.L.C. ("the Firm") through its publications, reports, newsletters, and communications, including but not limited to Investment News, Market Insight, and Investment Insight, are intended for informational and educational purposes only. These materials are not to be construed as specific investment recommendations or advice. DuLac Capital Advisory L.L.C. is a technical services management consultant for companies and institutional investors. DuLac Capital Advisory L.L.C. does not receive any revenue from any company or service mentioned in this insight piece.

**Not Investment Advice:**

The materials provided by the Firm do not constitute investment advice or recommendations to buy, sell, or hold any securities or investment products. The insights offered are general in nature and do not take into account the individual circumstances, investment objectives, risk tolerance, or financial situation of any particular institutional investor or recipient.

**No Reliance:**

Institutional investors should not rely solely on the information provided by the Firm for making investment decisions. It is recommended that investors conduct their own due diligence, seek advice from qualified financial professionals, and carefully consider their investment objectives and risk appetite before making any investment decisions.

**No Guarantee:**

While the Firm strives to provide accurate and up-to-date information, there is no guarantee of the accuracy, completeness, or reliability of the information provided. The financial markets and economic conditions are subject to change, and the information provided may become outdated or irrelevant over time.

**Risk Disclosure:**

Investing in financial markets involves inherent risks, and the value of investments may go up or down. Past performance is not indicative of future results. Institutional investors should be aware of the potential risks associated with investment decisions and should consult with professionals who are qualified to provide personalized investment advice.

**No Endorsement:**

Any mention of specific securities, investment products, or companies does not constitute an endorsement, recommendation, or promotion of those securities, products, or companies by the Firm. The inclusion of any such information is for informational purposes only. No compensation was received from including any investment product or technology into the White Paper.

**Legal and Regulatory Considerations:**

Institutional investors are responsible for understanding and complying with all applicable laws, regulations, and guidelines related to their investment activities. The Firm's materials are not intended to replace or substitute for legal or regulatory advice.

The Firm disclaims any liability for the use or interpretation of the information provided in its materials. Institutional investors should use their judgment and exercise caution when relying on any information provided by the Firm.

For personalized investment advice tailored to your individual circumstances, we strongly recommend consulting with licensed financial advisor at a major Wealth Manager.

All content published by DuLac Capital Advisory is Copyright Protected per U.S. law. Insight is protected speech and right to commerce per U.S. Constitution and Civil Rights Act of 1866, Civil Rights Act of 1871, and Civil Rights Act of 1964.