“Tragedy of the Net Zero Commons”— Identifying Investment Risk Factors and Hedging Opportunities

A Rockefeller, Mayor Bloomberg, and President Obama walk into a “Sustainable Bar” near Georgetown University… what do they order?

The Guinness Zero- Notre Dame legendary Quarterback, Joe Montana’s newfound drink of choice.

The line above may seem like a cringe-inducing beginning to a stand up routine at the comedy cellar in the Upper West Side, but like many jokes, there are some seeds of truth. On 02/09/2024, the Wall Street Journal published a story about how the Rockefeller Family Fund teamed up with Bloomberg Philanthropies to pressure the White House and Department of Energy to produce this LNG export ban[1].

Earlier in February 2024, the current U.S. Administration announced a ban on LNG exports from U.S. terminals. This announcement was a very surprising event risk to many institutional investors and public policymakers that have invested time and capital to the UN demands for the industrial implementation of the “transition to Net Zero” CO2 (“Carbon”) and GHG production.

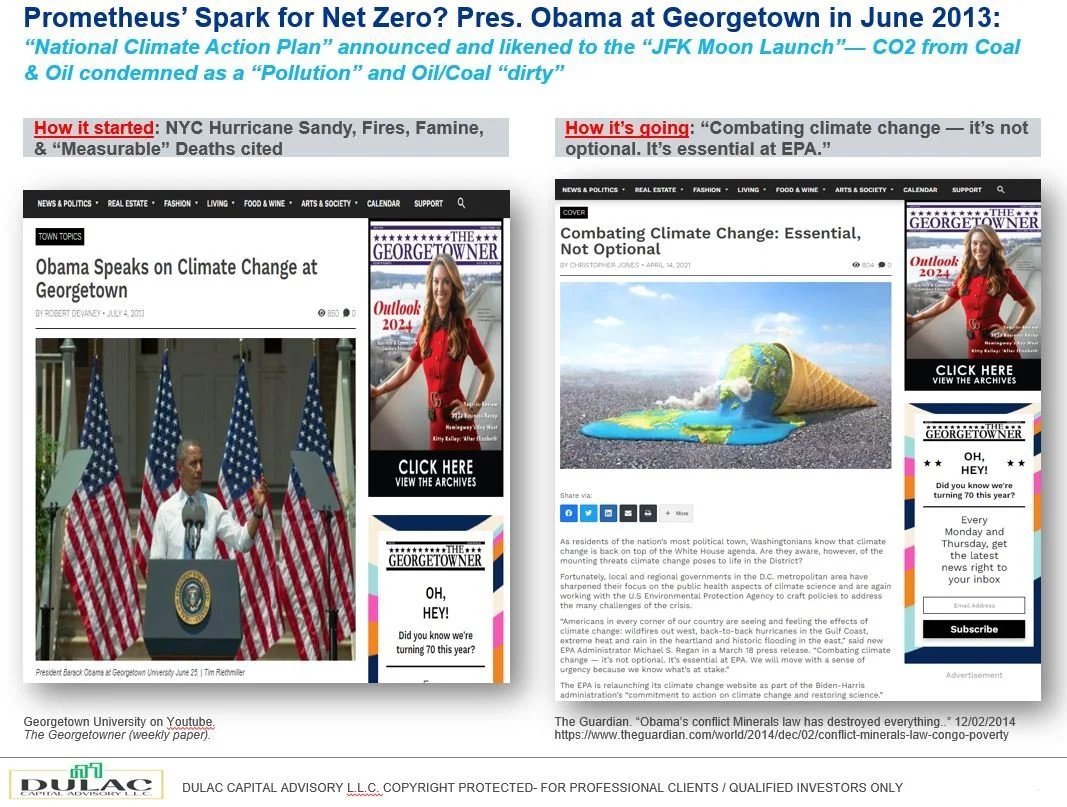

Tracing the arc for this Nat Gas ban though should not be a surprise to any investor that remembered President Obama’s speech at Georgetown University in 2013 where he announced the “new moon launch” of the 21st century would be the fight to stop “climate change” from “dirty” fossil fuel “pollution”—he called for marshaling investors, industry, and policymakers worldwide to transition economies to renewable energy.

Avoiding the “Road to Serfdom” on the Transition to “Net Zero”

The first two months of 2024 have provided some very interesting fodder for the debate between how much American capital should be forced by public policy fiat or explicit investment mandate to support DC’s commitment to the UN’s “Transition to Net Zero.” What portion that solar/wind/hydrogen should play in capital allocation—and what may impact their respective ROIC favorability—has become the $100 Trillion question.

There are tremendous event risks ahead on the “Road to Net Zero Transition” for both investment risk management and industrial capital investment—both will produce unintended consequences to traditional civil society if not managed correctly. The same happened with the fall out of the housing crisis between 2008-2013 after the previous decades mal-investment foray into the mortgage securitization market and institutional portfolio allocation process.

Uncertainty reveals pockets of opportunity. DuLac Capital Advisory L.L.C. thinks may be a keen time for many institutional investors and industrial capital planners to consider adjustments to help navigate their exposure away from unforeseen “Net Zero icebergs” while en route to the Paris Accord mandated Net Zero Transition by 2050.

However, this time for adjustments should not be viewed as a carte blanc elimination of all fossil fuel or related carbon-heavy industries— many are hedging this transition risk now with smart investments to CO2 offsetting technologies. Thus, this sealane should be examined as a possible entry point, within the right vehicle and capital structure considerations for the respective due diligence team.

Below is a summary of a few key recent news items that institutional investors must weigh into their medium term investment risk management process.

EPA as a Stakeholder in America’s Energy Markets with Soot regulation on Coal: USA EPA introduces new regulations to further limit “Soot” emissions within the coal industry—effectively adding another burdensome regulatory cost for the sake of ESG Goals: the WH stated the soot regulation will reduce Health Care costs by $55 Billion—yet provided no guidance on how to account for the clear ESG mandate per GAAP standards.

How the Rockefellers and Billionaire Donors Pressured Biden on LNG Exports: This is an important article to understand a tangible example of how Stakeholder Capitalism utilizes Sustainability Characteristics investing criteria, and DEI activists, to engage with policymakers and industry to influence outcomes within American capitalism: in effect, the stakeholder engagement creates a cycle where policy, capital markets, and social causes, all interact to influence the direction of Return on Invested Capital—it’s a “vicious” cycle for investors not part of the club.

Climate Politics Neuters an Energy Watchdog: WSJ features an article about how the current White House has a goal of banning all Nat Gas and Coal use in America by 2035. Additionally, the International Energy Agency (IAE) is now no longer modeling any potential of growth in fossil fuel demand in a couple of decades. (WSJ 02/14/2024.)

America’s Solar Industry is not as Productive as Mainland’s China: There is growing evidence that despite the Inflation Reduction Act tax credits and Infrastructure Act subsidies, the solar supply chain is increasingly being dominated by the People’s Republic of China.

This creates a possible hurricane of headwinds for institutional investors that must now contend with grassroots driven public policy mandates, while also balancing actual fiduciary investment risk management concerns: over-exposure to Mainland China due to trade war concerns, while also being mandated to invest in the “Net Zero Transition”—which has been supported by most of DC and NYC thought leadership.

Additionally, there are some institutional investors, such as New York State Commons Pension fund (source: Reuters 02/16/2024), that are now mandating increased exposure to renewables, while decreased exposure to large cap Oil companies—as they cite “Climate Change Risk” as now an investment concern.

DuLac Capital Advisory L.L.C. projects there will be growing fragmentation of public policy Energy Ecosystems in the United States—as each region ends up grappling with their own native energy demands, natural resource blessings, and unintended civic society consequences as global Net Zero Transition policies manifest themselves at the local level. This will create opportunities for institutional investors and industry planning experts that must hedge against the risk of “Global Green Inflation” and an over-reliance on PRC solar/wind supply chain.

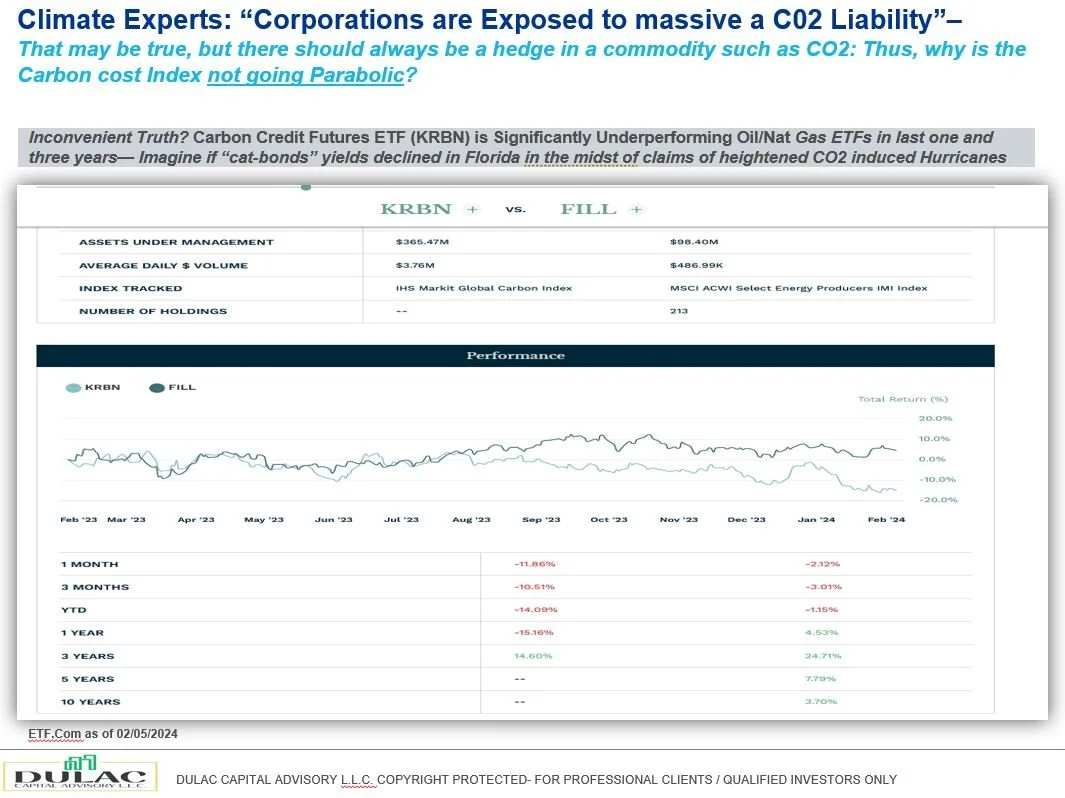

Why is the “Existential Risk of Climate Change” not translating to outperformance with the Climate Credit Futures Index ETF (KraneShares Global Carbon Strategy ETF: KRBN) vs. the Global Fossil Fuel Producer indexed based ETF (iShares MSCI Global Energy Producers ETF: FILL)—

Let alone massive AUM growth assuming the Efficient Market Hypothesis?

Oil and Nat Gas may be down—but they are not out:

Per the February 3, 2024 NY Times Dealbook article, U.S. large cap integrated oil companies generated strong profits in 4Q 2023. Despite the profit generation, strong balance sheets, and shareholder friendly capital plans, the market did not reward U.S. Oil and Gas in 2023 with either fund flows or multiple expansions.

The market is generally forward looking. DuLac Capital Advisory L.L.C. thinks that the market is thus requiring a lower than historic multiple on Oil/NatGas due to secular headwinds hitting the industry, rather than micro management risk factors. For example:

Costly regulatory “Net Zero Transition” compliance,

The increased “institutionalization” of explicit exclusionary investment constraints against Oil/NatGas— such as the NY State Pension February 2024 announcement; recall in 2020, many large Global Investment Banks announced their divestment from U.S. coal industry.

Potential increase in demand destruction as greater competition from PRC renewable supply chain proliferates globally.

The continued uncertainty from a GAAP accounting perspective of the alleged Carbon cost and attribution of production—especially on a cross-sector basis. For example, McKinsey & Co published a report in 2023 that cited the production of “gray ammonia” for agriculture fertilizer accounts for 450 Million Metric tons of CO2 per year. Yet, there are not many policymaker calls to divest from Large Cap Ag and its supply chain:

If there is a growing double standard against Oil and Nat Gas, institutional investors may therefore be pricing in the chance that American policymakers may indeed seek to turn much of America’s Oil and Nat Gas into a “stranded asset”—just like what has happened to U.S. Coal industry.

This all is generating a vicious cycle impacting the American energy supply chain’s resilience and independence from PRC. However, as astute investors know from studying Mandarin, the term for “risk”, also transposes to an analogy for “opportunity”.

DuLac Capital Advisory L.L.C. thinks active investors with strategic views that seek to support a future of American energy independence, yet still acknowledge the reality of the Tsunami that tens of trillions of Net Zero Transition mandates will cause by anyone completely “short” those regulatory/investment constraints, may find opportunity to structure investment risk factor exposure to the commodity producer risk factor in their portfolios. Why?

The market may be overly discounting, or not yet recognizing, their capital expenditures made to produce CO2 capture, storage, sequestration technologies (CSS). This technology development has been aided with “Inflation Reduction Act” tax credits, and the CSS distribution/storage/maintenance of CO2 production also generates Tax Credits that can be monetized as a tangible asset, as what First Solar recently did.

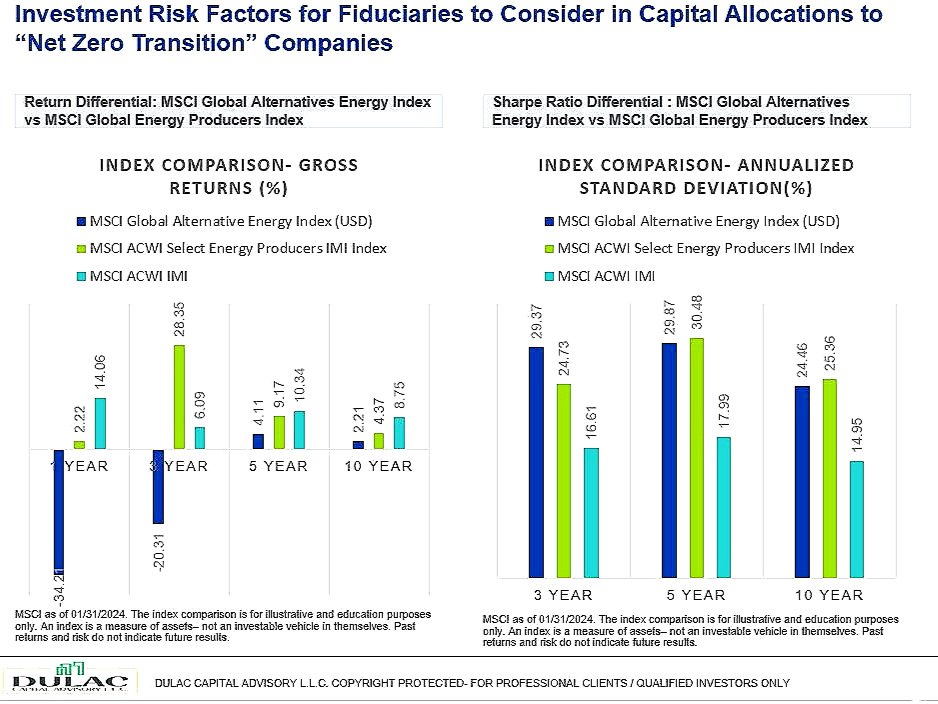

The Macro Commodity Risk Factor May be overpricing Downside Volatility of Large Cap IG Rated Integrated Oil

Despite trillions of incentives via US, EU, and UK taxpayer funds over the last 10 years, renewable stock indices are often not outperforming Oil/Nat Gas indices. However, investment flow to Oil/Nat Gas/Coal has been quite minimal in the Mutual Fund and ETF space— that indicates investor are willfully, thanks likely due to marketing/PR— avoiding the “dirty” fossil fuel sector, despite being largely asset rich and balance sheet strong: for example, look at the recently announced M&A activity within the O&G space, such as the Exxon with Pioneer announcement.

There is clear and present danger to American energy independence that the investment and regulatory restrictions may be placing on American fossil fuels, Materials Sector— it may not only impact investment risk-adjusted return profile, but also the nation’s industrial output.

If that seems doubtful— simply examine the low Price to Earnings or Enterprise Values to EBITDA that most American Coal, Nat Gas, and Oil now face. Despite profit growth and shareholder return of capital actions, the American, and international, fossil fuel industry has generally lagged behind in performance over the last ten years on a weighted average basis compared to industries deemed by MSCI as “less carbon intensive.”

Although there are still uncertainties as to how Industry will be forced to account for their alleged CO2/GHG exposure within a GAAP compliant manner, the trend is clear: there will be carbon taxes in the USA—just as there already are in European nations such as Norway. The question though will be—will they be explicit, or implicit? DuLac Capital Advisory L.L.C. thinks it is more likely that American fossil fuel and industrial companies will likely face greater chance of an implicit carbon taxes—which means the “toll” will be extracted via the capital markets, rather than direct levies from D.C.

Regardless, DuLac Capital Advisory L.L.C. believes now is an optimal time for institutional investors and industrial capital allocators must now start planning for this potential, and find hedging solutions to retain optionality for future growth. It does not mean divesting from Oil, Nat Gas, Steel, Ag, or even Coal—but rather finding ways to structure investment opportunities that leverage tax credits via the “Inflation Reduction Act”, GHG reducing Technological advances that large cap IG rated Fossil Fuel companies have invested in, and latent—or even policy declared “stranded” land assets and royalty rights of some fossil fuel companies….

Ryan Scott

Executive Director and Founder

DuLac Capital Advisory

(+1) 516-939-6833

Please reach out to DuLac Capital Advisory L.L.C. in the message box below for additional insight on what institutional investors and Think Tank policy researchers should consider to optimally navigate the choppy waters of Net Zero Transition.

Investment News, Market Insight, and Investment Insight Disclaimer

The information, investment news, and policy insights provided by DuLac Capital Advisory ("the Firm") through its publications, reports, newsletters, and communications, including but not limited to Investment News, Market Insight, and Investment Insight, are intended for informational and educational purposes only. These materials are not to be construed as specific investment recommendations or advice. DuLac Capital Advisory. is a technical services management consultant for companies and institutional investors. DuLac Capital Advisory does not receive any revenue from any company or service mentioned in this insight piece.

Not Investment Advice:

The materials provided by the Firm do not constitute investment advice or recommendations to buy, sell, or hold any securities or investment products. The insights offered are general in nature and do not take into account the individual circumstances, investment objectives, risk tolerance, or financial situation of any particular institutional investor or recipient.

No Reliance:

Institutional investors should not rely solely on the information provided by the Firm for making investment decisions. It is recommended that investors conduct their own due diligence, seek advice from qualified financial professionals, and carefully consider their investment objectives and risk appetite before making any investment decisions.

No Guarantee:

While the Firm strives to provide accurate and up-to-date information, there is no guarantee of the accuracy, completeness, or reliability of the information provided. The financial markets and economic conditions are subject to change, and the information provided may become outdated or irrelevant over time.

Risk Disclosure:

Investing in financial markets involves inherent risks, and the value of investments may go up or down. Past performance is not indicative of future results. Institutional investors should be aware of the potential risks associated with investment decisions and should consult with professionals who are qualified to provide personalized investment advice.

No Endorsement:

Any mention of specific securities, investment products, or companies does not constitute an endorsement, recommendation, or promotion of those securities, products, or companies by the Firm. The inclusion of any such information is for informational purposes only. No compensation was received from including any investment product or technology into the White Paper.

Legal and Regulatory Considerations:

Institutional investors are responsible for understanding and complying with all applicable laws, regulations, and guidelines related to their investment activities. The Firm's materials are not intended to replace or substitute for legal or regulatory advice.

The Firm disclaims any liability for the use or interpretation of the information provided in its materials. Institutional investors should use their judgment and exercise caution when relying on any information provided by the Firm.

For personalized investment advice tailored to your individual circumstances, we strongly recommend consulting with licensed financial advisor at a major Wealth Manager.

All content published by DuLac Capital Advisory is Copyright Protected per U.S. law. Insight is protected speech and right to commerce per U.S. Constitution and Civil Rights Act of 1866, Civil Rights Act of 1871, and Civil Rights Act of 1964.