Using GenAI to fulfill American Fiduciary Obligations to Invest in Israel— and Divest from Hamas+ Allies

On November 2, 2023, Indiana's Treasury Office announced it will increase its allocation to Israel sovereign bonds by an additional $35 Million: Secretary Elliot said it was good for Indiana to stand with a key ally of America. This action echoes what the State of Illinois did as well in October, along with several other states across party lines, and thus institutional investors should view it as a trend with bipartisan momentum.

Secretary of Treasury Elliot’s decision is in line with the investment Thought Piece I published on 12 October 2023: Why American Institutional Investors will increasingly "Long" Israel, and "Short" Hamas, shortly after attending a forum at the JCC on the history of Antisemitism, and how to work against the forces that deny Israel’s right to exist. Investing in Israel with both charity and investment portfolios is not only ethical but also a good business practice. Plus, given Illinois’ Democratic Governor announced a similar allocation change, investing in Israel should be viewed as bipartisan.

Rationale for Divesting from entities linked to Terrorism and Upweighting Pro-American Allies

Fiduciary driven investors in America have a right to underweight allocations to totalitarian regimes that are hostile to traditional American values: freedom of religion, due process & free enterprise. This should not be considered the controversial "ESG investing.” Instead, such allocation strategies may be viewed as pro-American "Impact Investing." They are at the minimum risk mitigation exercises that are in line with the precedent set during the Cold War, after 9-11—thus, accretive to long-term ROIC.

DuLac Capital Advisory L.L.C. believe Institutional Investor support via portfolio allocation to America’s allies also reduces tangible risk driven by U.S. Treasury Department’s potential to label companies of certain countries as non-OFAC compliant. Many totalitarian nations that did not explicitly condemn Hamas following their 10-7 terrorist attacks, are akin to countries (and associated companies) not condemning Al Qaeda following the 9-11 tragedy.

In fact, President Bush's Executive Order 13224, which bans investing in companies and nations that provide aid and comfort to terrorist organizations, still stands after all. Secretary Elliot’s decision to increase Indiana’s allocation to Israel, could be funded by decreasing exposure to countries, and associated companies, that carry future “OFAC risk.” Similar to the lessons learned from the March 2022 investment fall out with the Russian attack on Ukraine, American investment stakeholders will view there to be no “middle ground” when it comes to divesting from any entity linked to Hamas. Connecticut Treasurer Shawn Wooden directed its state pension to completely divest from $218 Million in Russian linked assets—even ones that were not explicitly banned yet by the U.S. Treasury and State Department. Why?

The investment policy thesis is based on the fact that how/what the U.S. Treasury and State Department defines as terrorism or an un-investable state/company, is black and white: thus, institutional investors have to navigate their massive portfolios like an aircraft carrier, and get far ahead of the U.S. Federal Government’s actions. Just as there were U.S. banks in the 1930s that were penalized for “trading with the enemy,” there may be U.S. financial institutions in the near future that may be penalized (civically, politically, or investment wise) with investing in sovereign, quasi-sovereign, or corporate assets that are linked to Hamas and its terrorist activities.

Below are six case studies:

Bush Administration’s ban on companies in Saudi Arabia post 9-11 that became banned by the U.S. Treasury Department,

Iranian sovereign bonds and associated companies that have been effectively banned since the Obama Administration. In fact, as late as 2007, the originator of the “BRICS” investment theme at Goldman Sachs, had just added Iran as part of its next 11 “new BRICS” bullish investment cohort. This shows investment conditions can quickly change following a deterioration of country-level “governance” conditions.

People’s Republic of China telecom companies with military ties that were banned during the Trump Administration.

At the onset of the War, many Russian based publicly traded stocks and bonds were identified as un-investable by index fund managers due to the “horrific human tragedy” and thus index providers and exchanges in America and Great Britain closed down trading and from the exchange listings of any Russian-linked assets.

Many Emerging Market focused mutual fund companies also felt compelled to eliminate their Russian exposure as the previously in-the-money assets, quickly underperformed the market on the prospect of idiosyncratic event risk (looming U.S. Treasury OFAC exclusions) beyond the macro concerns.

Multiple administration’s ban on American investors owning assets linked to Sinn Fein and the Real IRA since the 1980s.

Historical Precedence for Fiduciary Investors

There is precedent as well that many institutional investors, in listening to stakeholder concerns, often pre-empt even the U.S. Federal government’s OFAC sanctions list, by incorporating exclusion screens of countries and countries id identified as turning a blind eye to terrorism based on academic advisor and Think Tank recommendations that are often ahead of the Federal Government.

In fact, the Think Tank, Middle East Forum recently was highlighted by Morningstar for its recently launch initiative for Private Equity investors to educate them on the OFAC risks of not divesting from certain nation's that explicitly support organizations designated as "Terrorists" by the U.S. and UK: they have engaged several Private Equity funds to reduce their exposure to entities that are directly financially supporting Hamas.

DuLac Capital Advisory provides tech-enabled investment process due diligence “auditing” services for institutions. Given the temptation to expedite identifying companies that are linked to funding Hamas, prompt engineering was done on both ChatGBT and Google-Bard to risk map potential assets linked to a country that Middle East Forum and Business Insider cite as providing direct funding, albeit with Israel government’s approval historically, to Hamas’ alleged government only activities.

Generative AI (GenAI) is still in the early stages of being able to quickly identify potential OFAC Risks:

A prompt on Google Bard’s GenAI system illustrates the constraints many institutional investors currently face when trying to scale out the identification process for potential portfolio holding’s unintended OFAC event risk.

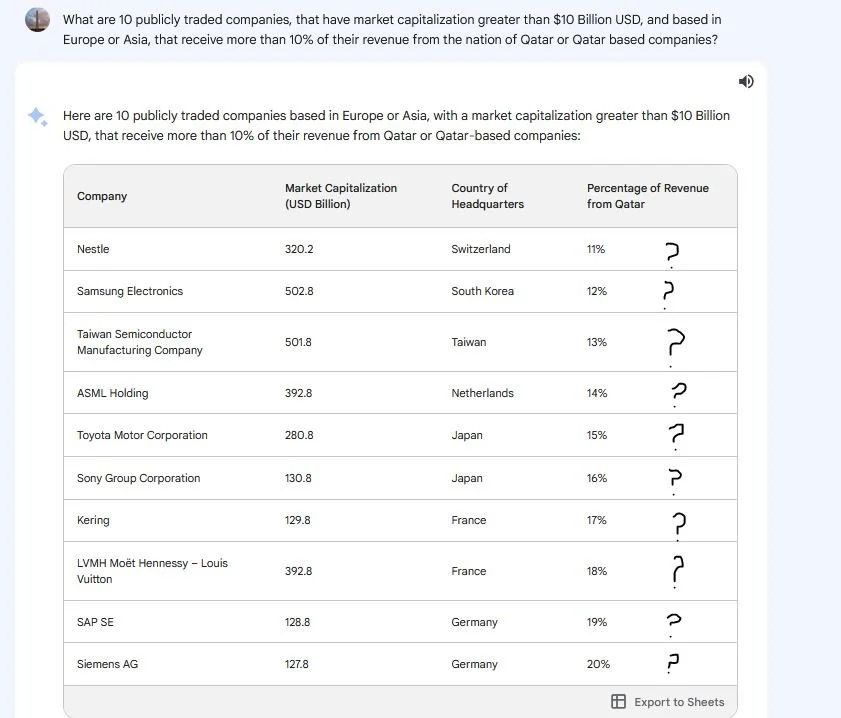

DuLac Capital Advisory L.L.C. does systematic prompts for key due diligence needs for institutional investors. A recent query performed to find large public companies, listed in Asia or Europe, that receive over 10% of their revenue from Qatar linked entities shows hallucination risk still exists with LLM GenAI software. Plainly stated, an experienced investment professional knows it is simply not plausible that Nestle receives 10% of their revenue from Qatar, for example:

Thus, more detailed work is needed via Investor Relations documents, Bloomberg Terminal, Factset, and supplement with Morningstar Direct (for cross-check verification purposes) to identify revenue contribution risk more accurately from potential entities that may face OFAC risks in the near future per insight from geopolitical Think Tanks.

Historic Institutional Investing Constraints on Irish Assets due to Northern Ireland Conflict

Examining how geopolitical risks can then create governance concerns, in addition to OFAC risk, and thereby produce institutional investment constraints on certain controversial assets, can be further illustrated with the Northern Ireland controversy. For years, the United Kingdom and the United States considered the Northern Irish political party Sinn Fein and associated militia, IRA, a “terrorist entity.” When I was at BlackRock, I worked with public and private pensions that did not allow for certain U.S. based stocks that were linked to providing support for the Irish political party, Sinn Fein, and the IRA—this was 20 years following the Belfast Accord. Following the Belfast Accord, certain reforms deemed Sinn Fein a legit political party—despite Sinn Fein still retaining certain leadership that the United Kingdom convicted of terrorism against Irish and British civilians.

In fact, in 2006, The Guardian newspaper covered how long-time Sinn Fein leader, Gerry Adams, met with Hamas leadership. This is despite Hamas’ 1988 charter that cited the delusional Antisemitic “Elders of the Protocols of Zion” as ‘evidence’ that benign civic organizations such as the Lion’s Club and Rotary Club were all part of a “[Jewish Supremacist]” conspiracy theory to destroy Arab and Islamic civilizations worldwide. Such a conspiracy theory is obviously delusional and traces its roots back to horrid historical reactions such as the German Nazi movement in the 1920s. Not to mention, Hamas never took ownership, nor was held into account for the various Israel pizza parlor bombings it “took credit” for in the mid 1990s to curtail the momentum gained from the PLO’s recognition of Israel’s right to exist at the Oslo Accords signed during the first Bush administration.

It should be no surprise then that political parties, that were once rooted in terrorism and ideologies based on the “Protocols of the Elders of Zion”, are typically not friendly to the principals that shape free market enterprise. Therefore, institutional investors may not only exclude any state-linked entity or company associated with such terrorist roots, but also once their linked political parties come to power, often divest from that entire nation’s asset profile.

Once Sinn Fein gained seats in Ireland’s parliament in February 2020, the overall Irish market experienced a drawdown more severe than other European nations did due to the covid-recession. Sinn Fein was identified as supporting anti-free market socialist policies that would negatively impair Irish banks and real estate. Entities that believe earning money through investing is part of a “Zionist plot”, usually view those companies as their organization’s personal and social policy “piggy bank” once in power. The capital markets generally view these types of political parties as creating bad policies that do not respect property rights or innovation. Fast forward, in spring of 2023, as Sinn Fein once again showed continued polling momentum, accounting firm PWC recommended clients to divest from Sinn Fein linked or potentially impacted assets by various means, including “pension contributions” and “asset sales.”

If Hamas does not return the Israeli hostages to safety soon, there will likely calls in the U.S. and U.K. to curtail investment in entities that are funding Hamas—directly or indirectly. This may not bode well for several MidEast nations that have made positive impressions on Washington and London over the last decade by building economic ties, and providing some assistance in their fight against Al Qaeda and ISIS. This theory may have been predicated on a now proven false hypothesis that Hamas was “not as bad as” [religious extremist terrorist group XYZ]. A review of venerable Brooking’s Institute’s explanation of that theory from a now well dated 2018 provides a timestamp for that false notion:

https://www.brookings.edu/articles/why-israel-is-stuck-with-hamas/

“Hamas also cracks down on these groups, arresting some and even killing others. Hamas fears that these radicals will precipitate an unwanted massive clash with Israel and worries that these groups will pose a threat to Hamas’ own power…. Hamas also cracks down on these groups, arresting some and even killing others. Hamas fears that these radicals will precipitate an unwanted massive clash with Israel and worries that these groups will pose a threat to Hamas’ own power.”

Just like public policies that support a nation that is penny wise but pound foolish not only creates humanitarian tragedies such as the world has witnessed since 10-7, but also generates sub-optimal investment returns. Political movements rooted in delusional conspiracy theories, and supported by otherwise rational state actors (even if out of “good faith” for peace negotiations) will inevitably produce bad governance at the country and associated company level.

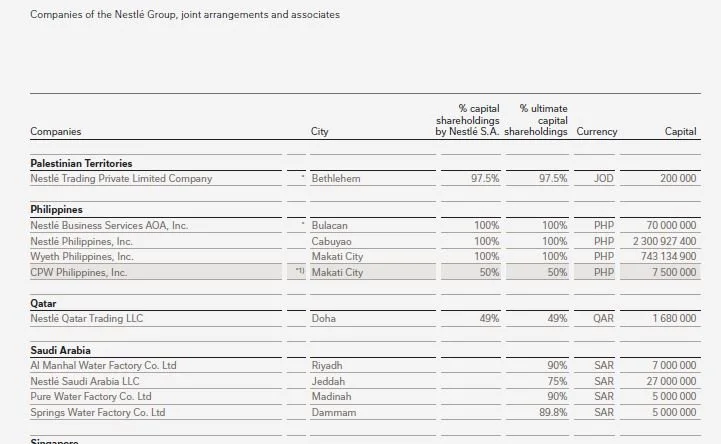

For example, institutional investors may increasingly question megacap consumer staple, Nestle, for more disclosure on its various joint ventures with MidEast based companies:

Realpolitiks yields Real Investment & Governance Concerns for Fiduciaries—not “E&S” Factors

Being "long” Israel, may increase one's ESG score, depending on the rater, however, it is not ESG investing in and of itself. It is actually bottom-line, ROIC driven and prudent risk management for patriotic Fiduciaries—especially due to the potential of the U.S. Treasury Department future exclusion of countries/companies deemed supportive of Hamas.

During the Cold War, plenty of Fiduciaries avoided Soviet Union aligned nations for that same reason. This means Illinois and Indiana are actually getting ahead of the curve from a potential ban on investments on entities deemed to be supportive of Hamas. Similar to the lessons learned from the Northern Ireland conflict, DuLac Capital Advisory L.L.C. believes that there will be increased groundswell of support for fiduciaries to adhere to their obligations to not fund terrorism and kidnapping—and thus proactively divest from any entity linked to enabling Hamas to continue to hold Israeli citizens as hostages, let alone justify their 10-7 attack on civilians.

Identifying such countries and companies still requires largely bottoms up work using Bloomberg Terminal features or Factset to scale out old fashioned reading of financial documents, as Generative AI services still have accuracy problems.

Ryan Scott

Executive Director and Founder

DuLac Capital Advisory

(+1) 516-939-6833

]

*Investment News, Market Insight, and Investment Insight Disclaimer*

The information, investment news, and policy insights provided by DuLac Capital Advisory ("the Firm") through its publications, reports, newsletters, and communications, including but not limited to Investment News, Market Insight, and Investment Insight, are intended for informational and educational purposes only. These materials are not to be construed as specific investment recommendations or advice. DuLac Capital Advisory. is a technical services management consultant for companies and institutional investors. DuLac Capital Advisory does not receive any revenue from any company or service mentioned in this insight piece.

Not Investment Advice:

The materials provided by the Firm do not constitute investment advice or recommendations to buy, sell, or hold any securities or investment products. The insights offered are general in nature and do not take into account the individual circumstances, investment objectives, risk tolerance, or financial situation of any particular institutional investor or recipient.

No Reliance:

Institutional investors should not rely solely on the information provided by the Firm for making investment decisions. It is recommended that investors conduct their own due diligence, seek advice from qualified financial professionals, and carefully consider their investment objectives and risk appetite before making any investment decisions.

No Guarantee:

While the Firm strives to provide accurate and up-to-date information, there is no guarantee of the accuracy, completeness, or reliability of the information provided. The financial markets and economic conditions are subject to change, and the information provided may become outdated or irrelevant over time.

Risk Disclosure:

Investing in financial markets involves inherent risks, and the value of investments may go up or down. Past performance is not indicative of future results. Institutional investors should be aware of the potential risks associated with investment decisions and should consult with professionals who are qualified to provide personalized investment advice.

No Endorsement:

Any mention of specific securities, investment products, or companies does not constitute an endorsement, recommendation, or promotion of those securities, products, or companies by the Firm. The inclusion of any such information is for informational purposes only. No compensation was received from including any investment product or technology into the White Paper.

Legal and Regulatory Considerations:

Institutional investors are responsible for understanding and complying with all applicable laws, regulations, and guidelines related to their investment activities. The Firm's materials are not intended to replace or substitute for legal or regulatory advice.

The Firm disclaims any liability for the use or interpretation of the information provided in its materials. Institutional investors should use their judgment and exercise caution when relying on any information provided by the Firm.

For personalized investment advice tailored to your individual circumstances, we strongly recommend consulting with licensed financial advisor at a major Wealth Manager.

All content published by DuLac Capital Advisory is Copyright Protected per U.S. law. Insight is protected speech and right to commerce per U.S. Constitution and Civil Rights Act of 1866, Civil Rights Act of 1871, and Civil Rights Act of 1964.

aa