Turkey Tantrum— Institutions May Start Taking “Chips off the Table” for MSCI Turkey Index Exposure

Risk Factor Considerations for American Institutional Investors Concerned with Turkey’s Potential OFAC Risk in Light of U.S. BDS Mandates & BlackRock Deal with Kingdom of Saudi Arabia

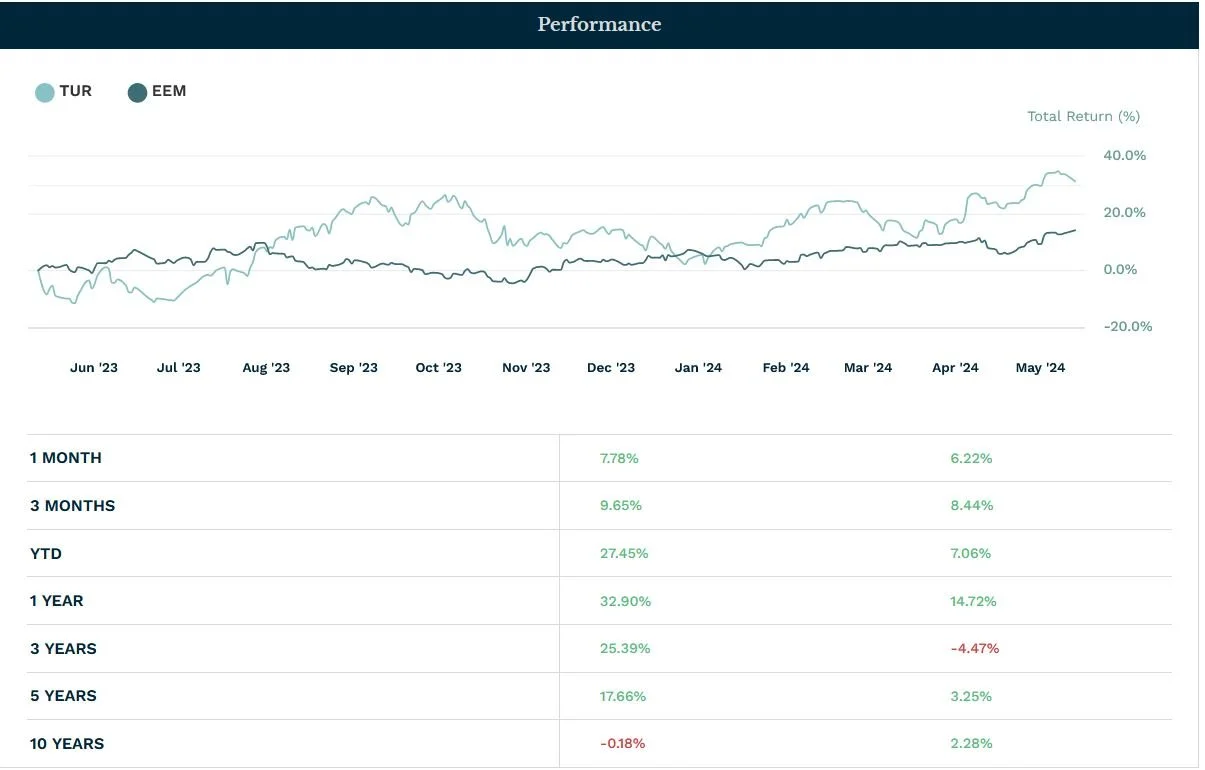

MSCI Turkey IMI Index is one of the best performing Emerging Market cohorts YTD: benefiting from declining inflation & better financial conditions vs. 2023. However, fiduciary risk management requires steering the ship way ahead of the icebergs.

As 400 Million people of the Eastern Orthodox Christian Church are in the early stages of their Easter season, it is becoming apparent that many institutional investors may have to counter-intuitively consider “abstaining” from Turkey— the country’s markets, not the poultry—as a vehicle to reduce asymmetric geo-economic risks associated with the Middle East & Ukrainian war for sovereignty. Many American 401ks, university endowments, and pensions have exposure inadvertently to Turkey via Broad Emerging Market index funds, or benchmarks hugging “active funds”.

This is an important memo for anyone seeking to connect the dots on how this unintended over exposure to underperforming foreign assets, may also be aiding unproductive geopolitical strategy for the U.S. to implement peace in Mideast, and for the EU to stem the root cause of “migration” via illegal ports of entry.

Erdogan, Armenia and the land of Aristotle-

Per American Think Tank, Middle East Forum, Turkey leadership recently boasted about the prospect of invading Greece: Turkey once occupied Greece for a couple hundred years— America supported Greece independence in a bygone era. Additionally, Middle East Forum pointed out in a February 2024 insight note that Turkey has experienced some compliance challenges in terms of nipping ISIS-K financial/logistics infrastructure in the bud— especially vis a vis Sberbank (an OFAC non-compliant Russia bank entity). This all became even more glaringly problematic considering the tragic attacks against Russia by ISIS-K (per U.S. State Department) on 22 March 2024.

Today, Catholic News Agency reports Turkey’s government is “converting” an ancient Byzantine Era Orthodox Christian Church, which England Stewarded as a Museum post WWII, into a “Mosque.”

Why does this matter?

Per the WSJ, when US Sec of State Blinkin met with Turkey’s President in 4Q 2023 to discuss support for Israel post 10-7 tragedy, Turkey’s leader oddly charged Israel’s PM as being “richer than a [evil 1930s German Antisemitic Dictator]”. It was a clear signal that Turkey sought a “have a cake and eat it too strategy” on the latest Middle East turmoil.

Remember, Turkey was once the seat of the Eastern (Byzantine) Holy Roman Empire from 400 AD till around 1492 AD. It was a center of trade to Persia/Africa/China, intellectual advancements, and an “ambassador zone” of Western Civilization to the east.

Today, many investors are wondering whether it’s worth even owning EM equities from a utility basis using broad “passive” exposure vehicles: the evidence is pointing to NO. Outside of a few pockets such as the tech ecosystem to the Taiwanese industry in Taiwan (Republic of China), there simply is far too much “government risk” that translates to company governance downside risk. Russia is a poster child for this dynamic.

MSCI EM IMI index after all has generated only a 0.17 Sharpe Ratio over the last Ten Years— less than 1/3rd as the MSCI USA IMI index (source: MSCI.com as of 01/31/2024). Basically, a teenage son who has a history of higher risk on the road, and more dents on the car— typically doesn’t get to drive the new BMW 535 EV once it’s dark out. However, this year, MSCI Turkey has been a standout: producing an outsized positive contribution to MSCI EM’s absolute and risk factor adjusted (as indicated by Sharpe Ratio) in 2024 (source: MSCI as of 04/30/2024). However, for prudent institutional investors, there are emerging factors which indicate this may be a prudent time to take some chips off the table in regards to Turkey beta exposure, and find a “chair to sit on” even while the music is playing in regards to broader MSCI Middle East & North Africa equity risk.

DuLac Capital Advisory think institutional investors will increasingly view that It is getting quite dark in Turkey and much of its other implicitly antisemitic state Allie’s around the world. They underprice OFAC EVENT RISK and/or 26 American States’ various “Anti-BDS” institutional investment policy laws at their own peril.

Historically, once an emerging market nation’s leadership begins to act in an uncivil manner per international standards, that should be viewed as a potential canary in the coal mine of greater risk to come to its corporations.

Additionally, given Turkey’s longtime President’s recent announcement of its intent to Ban, Divest, and Boycott from Israeli commerce, Turkey equities for beta exposure may become increasingly fraught with State “Anti-B.D.S.” laws in the United States of America.

Below is an 8 Point summary on under appreciated risk factors for Turkey exposure— which can be extrapolated to other non

Why does this matter for fiduciary bound investors in this era of Geopolitical and Technological Fragmentation?

1. Turkey is a net importer of commodities: they risk upsetting further its relationship with Orthodox Russia— as the WSJ has reported has been able to sell its oil and coal to Turkey, which it then “flips” to sanction bound countries. Worsened relations with Russia May elevate Turkey’s commodity price inputs, inducing stagflation.

2. Turkey erodes soft power and good will as an asset in the West: Turkey would lead a boycott within the UN ecosystem against the US, The Netherlands or Israel if a Mosque was “converted” to a Tech Center, JCC, let alone classical Christian European Art Museum. Perhaps though Turkey’s leadership is doing such “conversion” to appease the Global Antisemitic Crowd— it didn’t end well for those three Ivy League Presidents. Recall in 2014– when President Obama took the eye off the modest ball and ISiS took over American hard won Fallujah— Turkey did a deal with “ISIS” (for some reason BHO insisted on calling the evil organization “Isil”) to release few dozen Turkish hostages.

3. Such “cultural boycott” asymmetric risk creates an imbalance of “soft power”— a key driver for America’s effort to gain global market share during the Cold War. In the mad dash for solar/wind resources on Latin America (90% Christian) and Congo (99% Christian), Turkey’s actions force America and UK to spend political capital in order to enforce Cold War norms— otherwise face the fate of being viewed as “paper tiger” which will drive up “renewable resource” costs for the U.S. sphere.

3. Who cares of this is the real investment policy age that has declared “Climate Change” as the greatest “Existential Risk”? My firm is skeptical on the (UN COP28/EU/DC and PRC supported) driven global legal regulations and investment policies that have now allocated $100 Trillion to “Net Zero Transition” as a mechanism to stop “existential climate risk.” However, such a sizable centrally planned earmarked capital allocation cannot be ignored: it’s a major tidal wave that all investors must navigate. Turkey’s actions makes it being at risk of an “uncovered short” against this Global Green Renewable Inflationary Tsunami.

5. Turkey is a net importer of energy and “renewable minerals”— thus its “cultural Cold War actions” may end up driving up its exposure to “Global Green Inflation” cost input risks even further. Since ~22% of Turkey equities are Industrials, this would has not portend well for their operating profits. (Source: MSCI as of 01/31/24). Turkey though could benefit from a more constructive relationship with U.S., EU, Israel, and Kingdom of Saudi Arabia (which just entered a joint venture with BlackRock for a wholly domiciled KSA subsidiary of BlackRock staffed with local investment professionals) that would enable Turkey to reduce its net energy expense— on a CO2 Adjusted basis— via Carbon Storage Tech partnerships & renewable supply chain deals.

6. There is a Net Zero policy mismatch vs the investment reality: PRC economic sphere, which Turkey is part of, dominates the renewable energy supply chain. WSJ reported in February that the PRC has 44% lower costs for solar panel production. Additionally, it’s EV car leader, BYD, now eclipse TSLA for total cars produced: and is even going up chain for the premium market. Conversely TSLA is seeking to produce $30K EVs. Remember, PRC allowed TSLA to open a factory in Beijing to produce the Model Y; meanwhile PRC’s BYD just opened a factory in Turkey’s historic rival, Hungary. This means Turkey could end up being the odd man left out unless it forges a more constructive commercial relationship with the U.S. and EU Sphere.

7. Immigration, Migration, and Productivity: Over the last 40 years, there generally has been a high tolerance in the West for supporting immigration and refugees, even if they come in through illegal ports of entry and unproven claims for refugee status. Given the budget gaps many states in America faces, the NHS chronic budget gap in London now faces, and EU budget shortfalls due to “migrant assimilation challenges”, it is becoming clear to smart active investors that the productivity gains for unfettered immigration are much lower than in the Industrial Age of America.

8. This means means there is heightened risk for “Intra-Border Clash of Civilizations” (see: Dr. Samuel Huntington) as the West realizes the current cohort of immigrants, may want to apply the “Turkey cultural conversion standards” even within European domiciled traditional cultural assets.

Location, Location, Location— Emerging Turkey Beta Exposure Risk in light of National Security Realities

In other words, per classical portfolio management, it doesn’t make sense to add higher volatility and lower return producing assets to one’s portfolio— unless there is some type of macro or management catalyst that points to the asset will soon experience an upside catalyst. Turkey’s closure of ancient Orthodox Churches when Orthodox Russia, threats against Greece (per Middle East Forum), and its leadership’s unhelpful stance with the EU on Muslim immigration and Israel regarding Gaza, are not signs of decreased systemic risk.

Finally, from a National Security risk: why would a Marine from Oklahoma, who attends Pastor Hagee’s Church, for example, ever want to support Turkey— a nation closing down Churches and acting in an antagonistic manner against Israel— under Article 5? It is likely America policymakers may take notice. This is doubly so given half of American States have “Anti BDS” laws; which means their State Pensions (and University Endowments downstream) are prohibited from investing in entities that carte blanc Divest or Boycott Israel commerce. Turkey has indeed reached that fork in the road, and therefore American institutions may find it an optimal time to start pumping the breaks on their beta Turkey exposure.

Please reach out on any questions via the message box below.

Ryan Scott

Executive Director and Founder DuLac Capital Advisory (+1) 516-939-6833

Sources:

https://www.msci.com/documents/10199/97e25eb7-9bd0-4204-bea9-077095acf1d3

https://www.msci.com/documents/10199/2a599370-f52b-aad6-adb0-29e366bb9d4d

https://www.msci.com/documents/10199/4211cc4b-453d-4b0a-a6a7-51d36472a703

https://www.meforum.org/65551/turkey-threatens-to-invade-greece-and-armenia

Investment News, Market Insight, and Investment Insight Disclaimer

The information, investment news, and policy insights provided by DuLac Capital Advisory ("the Firm") through its publications, reports, newsletters, and communications, including but not limited to Investment News, Market Insight, and Investment Insight, are intended for informational and educational purposes only. These materials are not to be construed as specific investment recommendations or advice. DuLac Capital Advisory. is a technical services management consultant for companies and institutional investors. DuLac Capital Advisory does not receive any revenue from any company or service mentioned in this insight piece.

Not Investment Advice:

The materials provided by the Firm do not constitute investment advice or recommendations to buy, sell, or hold any securities or investment products. The insights offered are general in nature and do not take into account the individual circumstances, investment objectives, risk tolerance, or financial situation of any particular institutional investor or recipient.

No Reliance:

Institutional investors should not rely solely on the information provided by the Firm for making investment decisions. It is recommended that investors conduct their own due diligence, seek advice from qualified financial professionals, and carefully consider their investment objectives and risk appetite before making any investment decisions.

No Guarantee:

While the Firm strives to provide accurate and up-to-date information, there is no guarantee of the accuracy, completeness, or reliability of the information provided. The financial markets and economic conditions are subject to change, and the information provided may become outdated or irrelevant over time.

Risk Disclosure:

Investing in financial markets involves inherent risks, and the value of investments may go up or down. Past performance is not indicative of future results. Institutional investors should be aware of the potential risks associated with investment decisions and should consult with professionals who are qualified to provide personalized investment advice.

No Endorsement:

Any mention of specific securities, investment products, or companies does not constitute an endorsement, recommendation, or promotion of those securities, products, or companies by the Firm. The inclusion of any such information is for informational purposes only. No compensation was received from including any investment product or technology into the White Paper.

Legal and Regulatory Considerations:

Institutional investors are responsible for understanding and complying with all applicable laws, regulations, and guidelines related to their investment activities. The Firm's materials are not intended to replace or substitute for legal or regulatory advice.

The Firm disclaims any liability for the use or interpretation of the information provided in its materials. Institutional investors should use their judgment and exercise caution when relying on any information provided by the Firm.

For personalized investment advice tailored to your individual circumstances, we strongly recommend consulting with licensed financial advisor at a major Wealth Manager.

All content published by DuLac Capital Advisory is Copyright Protected per U.S. law. Insight is protected speech and right to commerce per U.S. Constitution and Civil Rights Act of 1866, Civil Rights Act of 1871, and Civil Rights Act of 1964.